Consumer-Permissioned Verifications: What They Are & Why They Matter

Income, employment, and asset verifications have long been a burden for both applicants and the organizations that serve them. Whether someone is applying for a mortgage, rental housing, or government benefits like Medicaid or SNAP, proving income, employment, and assets typically means one of two things: tracking down paystubs, W-2s, bank statements, and other documentation or relying on a verification database like The Work Number.

Consumer-permissioned data—also known as consent-based verification (CBV)—is changing that dynamic. By putting individuals in control of their own information, this approach streamlines verification, reduces costs and administrative burden, and creates a more transparent, ethical system for data sharing.

What is consumer-permissioned (consent-based) data?

Consumer-permissioned data is exactly what it sounds like: information that individuals actively authorize others to access. Rather than having their data bought, sold, or shared without their knowledge, individuals decide when, how, and with whom their personal information is shared.

In terms of income, employment, and asset verifications, this means that when someone applies for a service—whether it's a loan, housing, or government benefits—they can connect directly to their employer, payroll, or banking platform and grant temporary access to their income, employment, and asset data. The process typically takes just a few clicks, and applicants maintain complete control over their data, including the ability to revoke access at any time.

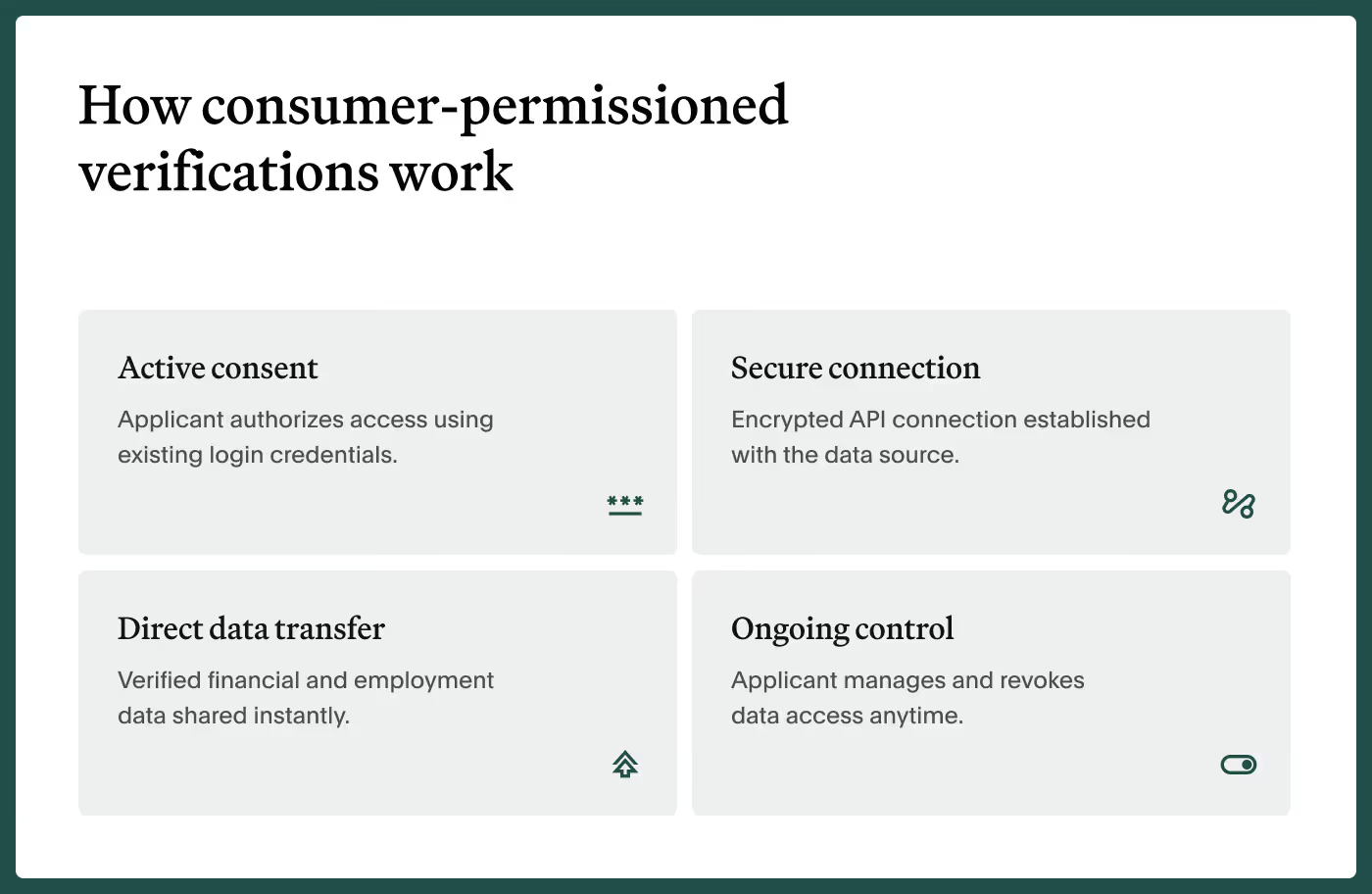

How consumer-permissioned (consent-based) verifications work

The consumer-permissioned verification model follows a straightforward process:

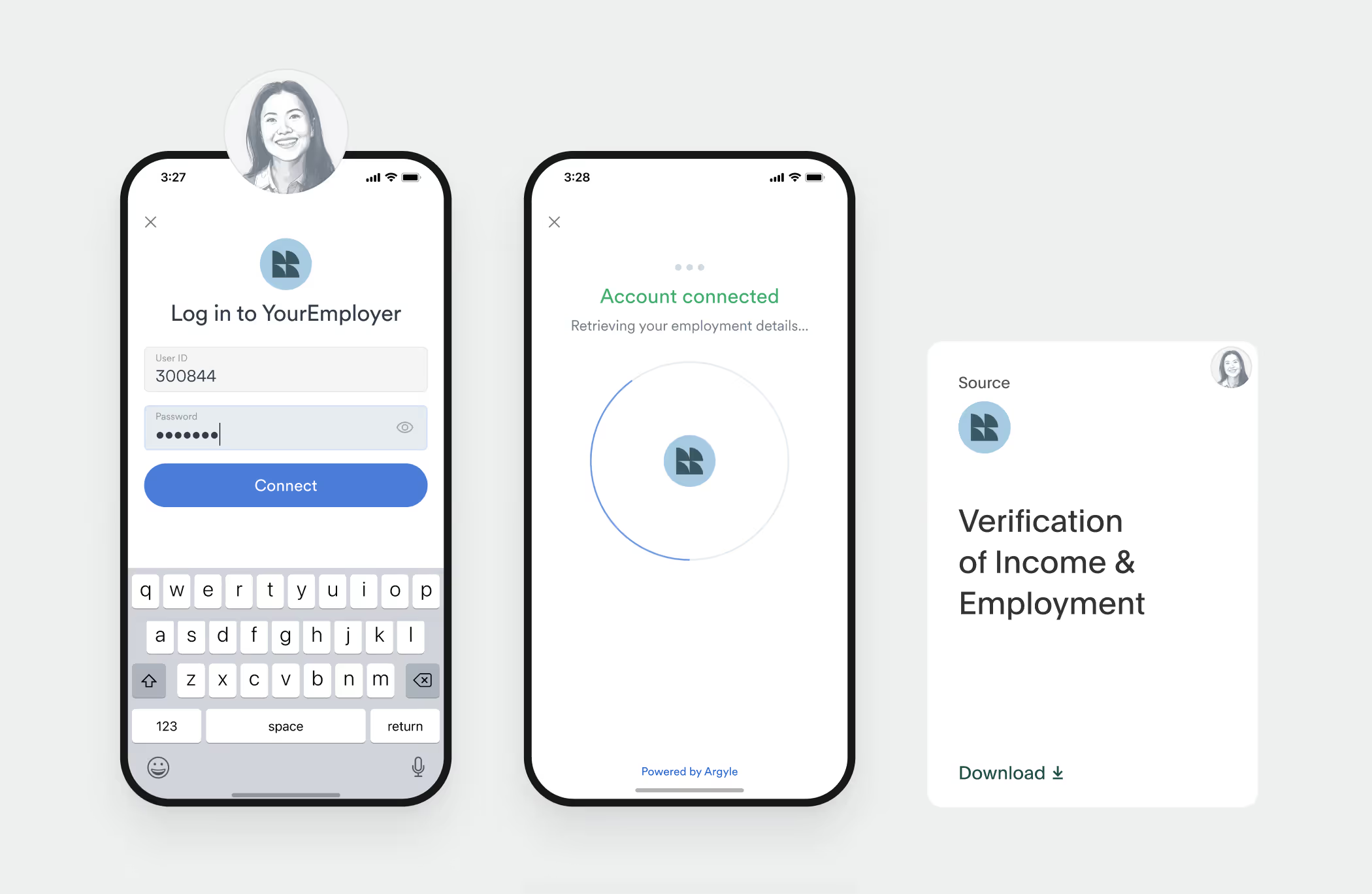

- Active consent: The applicant selects their employer, payroll provider, or financial institution from a comprehensive database and logs in using their existing credentials—the same ones they use to view their paystubs.

- Secure connection: Once authenticated, a secure API connection is established between the employer, payroll provider, or financial institution and the service provider or government agency.

- Direct data transfer: Income, employment, and/or asset information flows directly from the source to the authorized service provider in real time, eliminating the need for manual document collection.

- Ongoing control: The applicant can monitor which service providers have access to their data and revoke permissions whenever they choose.

This model represents a fundamental shift in how personal data is handled—from an opaque system where data is aggregated and resold to a transparent one where individuals are active participants.

Consumer-permissioned (consent-based) verifications vs. traditional database methods

Traditional verification databases work by buying and aggregating employment and income data from employers and payroll providers, and then making it available to service providers for a fee. This happens largely without applicants’ knowledge or meaningful consent. Instead, their data is collected, stored, and sold behind their backs.

This model creates several problems:

- Lack of transparency: Applicants typically don't know their data has been collected, who has access to it, or how it's being used.

- Limited coverage: Database providers only have information from participating employers. The Work Number, for example, has significant coverage gaps—particularly for gig workers, small business employees, and federal government workers.

- Data staleness: Information in databases may be weeks or months old, leading to inaccurate verifications that can delay approvals or result in wrongful decisions.

- High costs: The buy-and-sell model makes traditional database verification reports expensive, with costs that add up quickly when agencies need to verify thousands of applicants or conduct periodic reverifications.

- Privacy concerns: The practice of buying and selling applicants’ personal data without their knowledge has drawn criticism from consumer advocates and regulators, including the Consumer Financial Protection Bureau (CFPB).

The consumer-permissioned (consent-based) approach

Consumer-permissioned verifications solve these problems through direct-source connections that applicants knowingly and voluntarily consent to.

- Transparency: Individuals know exactly what information they're sharing, with whom, and for how long. They can view their active connections and data sharing history at any time.

- Coverage for more income types: Because consumer-permissioned platforms establish direct connections with employers and payroll providers, they can access data for a much broader range of applicants—including those who work in the gig economy, for small businesses, and for the government.

- Real-time accuracy: Data comes directly from the source in real time, ensuring service providers work with the most current and accurate information possible.

- Lower costs: Consumer-permissioned verification is significantly more cost-effective than traditional database methods, with some providers offering up to 80% savings, like Argyle, compared to The Work Number.

- Ethical data practices: Individuals' data is never bought, sold, or stored indefinitely. It's shared only with their explicit permission and deleted according to clear retention policies.

The benefits of consumer-permissioned, consent-based verifications

The shift to consumer-permissioned data creates advantages for everyone involved in the verification process.

Applicants benefit from a faster, easier process that respects their privacy and puts them in control. Instead of scrambling to find paystubs or waiting weeks for their employer to respond to a verification request, they can complete verification in minutes. This is especially valuable for:

Service providers and government agencies that verify income, employment, and assets see dramatic operational improvements. In addition to lower costs and higher accuracy, they experience faster processing times, with verification happening in minutes rather than days or weeks. There is also the benefit of reduced administrative burden. Caseworkers and loan officers spend less time chasing documentation and can focus on higher-value activities.

For government agencies in particular, consent-based verifications offer a path forward in an environment where agencies are being asked to do more with less—to conduct more frequent income checks, implement work requirements, and maintain program integrity while facing budget constraints and staffing challenges.

Addressing common concerns

As with any new approach, consumer-permissioned data raises questions. Here's how the model addresses common concerns:

"Do applicants even know their payroll passwords?"

This is one of the most common questions about consumer-permissioned verifications.

Leading consumer-permissioned verification platforms like Argyle offer several solutions to ensure high conversion rates regardless of password knowledge:

- Passwordless login: Many payroll systems now support login using personal characteristics like name, email, and phone number instead of passwords. This option allows individuals to verify their identity without needing to remember a password they may use infrequently.

- Single sign-on (SSO) integration: Argyle supports 65+ SSO providers, including the top 15 by market share (Microsoft, Okta, OneLogin, Google, PingIdentity, and others).

- Password manager compatibility: Argyle integrates seamlessly with password managers for select employers, allowing people to auto-fill credentials they've saved without needing to manually recall them.

- Built-in password reset: If someone doesn't remember their password, Argyle ensures they never have to leave the verification experience to reset it and gain access.

- Document upload as fallback: For the small percentage who still can't connect digitally (or choose not to), instant document upload tools allow them to submit paystubs, W-2s, or other proof of income as an alternative.

By offering multiple pathways to authentication rather than a one-size-fits-all approach, consumer-permissioned platforms like Argyle ensure that password knowledge isn't a barrier to quick, easy verification.

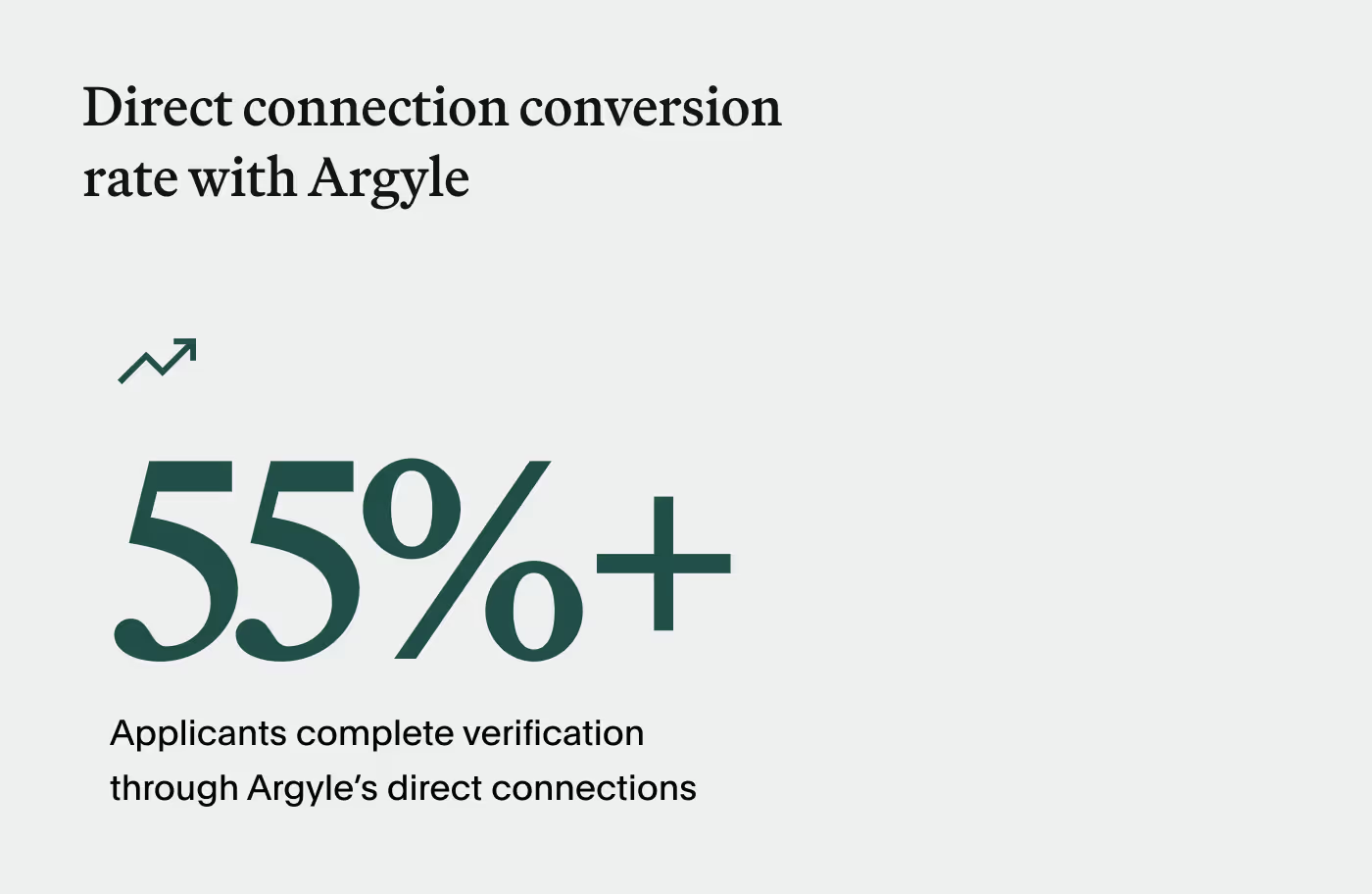

"What if someone doesn’t want to connect their accounts?"

Consumer-permissioned verification is always voluntary. Individuals who prefer not to connect their accounts can still submit traditional documentation like paystubs or W-2s. However, the majority of people choose to connect when given the option because it's faster, easier, and gives them more control than the alternatives.

Argyle, for example, achieves direct connection conversion rates of 55% or higher—meaning that when given the option, more than half of applicants successfully complete verification through direct connections.

"What happens to an applicant’s data after verification?"

Reputable consumer-permissioned platforms have clear data retention and deletion policies. With Argyle, for example, consumer data is made available to service providers for 30 days after the end of the service agreement, and then it's permanently removed from servers. The data is never aggregated, resold, or repurposed for other uses.

Applicants can also revoke access to their data at any time through user control centers like Argyle Passport, giving them ongoing authority over their information long after the initial connection.

The future of verification

Consumer-permissioned data represents the future of income and employment verification—one where transparency, accuracy, and individual control are the standard rather than the exception.

The question isn't whether to adopt consumer-permissioned data, but when. Those who move early will begin reaping the benefits sooner: lower costs, happier applicants and clients, more accurate data, and a verification process that's ready for the future.

Ready to explore how consumer-permissioned data can transform your verification process?

Contact Argyle to learn how our direct-source, consent-based verification platform can help your organization reduce costs, improve accuracy, and put individuals in control of their data.