HELOCs Are Booming, But So Is Risk. It’s Time Verification Caught Up

After years in the background, HELOCs have surged back to the center of the mortgage industry, and for good reason.

With homeowners locked into low-rate first mortgages, tapping equity through a second line has become one of the only sensible ways to access capital. Total HELOC and home equity origination volume grew 7.2% in 2024, and the Mortgage Bankers Association expects HELOC debt outstanding to grow another 9.8% in 2025 and 9.5% in 2026. Meanwhile, Q1 2025 second lien equity withdrawals hit nearly $25 billion—the largest first-quarter volume in 17 years.

But there’s also a growing disconnect between how fast this market is expanding and how carefully lenders are evaluating who they’re lending to. Given the economic environment we're operating in, that disconnect deserves a harder look.

The assumptions that built this market no longer hold

HELOCs were historically underwritten with a relatively light touch on income. If you owned a home, had built substantial equity, and had a high FICO score, you were considered a reasonable risk. The asset backing the loan provided a meaningful cushion. Collateral was king.

That calculus worked well in a low-unemployment, rising-equity environment. But we’re no longer in that environment.

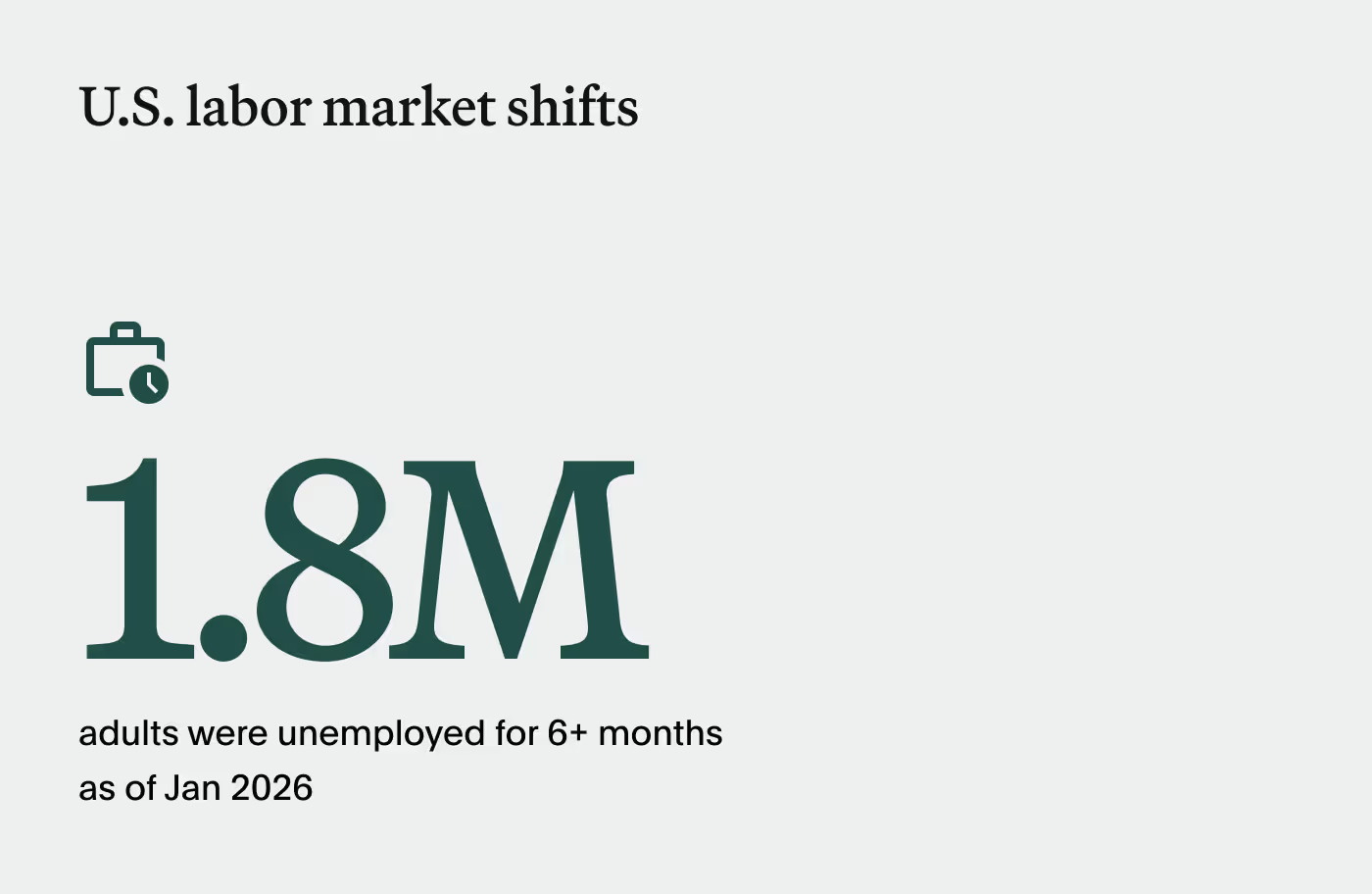

The U.S. labor market has shifted materially over the past 12 to 18 months. While the economy added 130,000 jobs in January 2026, the broader trend is harder to dismiss: 2025 was the weakest year for job growth since 2020, and unemployment climbed to a four-year high of 4.6% in November before edging back to 4.3% in the latest jobs report.

More telling than any single month’s headline number is what's happening beneath the surface: Long-term unemployment—a particularly meaningful indicator of structural labor market stress—has been climbing steadily for the past three years. As of January 2026, 1.8 million U.S. adults had been unemployed for at least 6 months.

At the same time, the borrower profile for HELOCs is changing. The MBA's data shows debt consolidation now accounts for 39% of HELOC origination volume in 2024, up from just 25% two years earlier. That’s a significant shift. The renovating homeowner who takes out a HELOC to build a new kitchen looks very different from a borrower who is tapping home equity because their non-housing debt has become unmanageable. And that second borrower—financially stretched and potentially over-leveraged in a weakening job market—is increasingly the person on the other side of HELOC transactions.

Stability isn’t immunity

To be fair, Experian's recent risk analysis confirms that HELOCs have continued to show relative stability through mid-2025. But that same Experian report is explicit on this point: Stability should not be mistaken for immunity. Elevated consumer debt, persistent inflationary pressure, and a softening labor market “could introduce risk into home equity portfolios with little advance notice.”

The leading indicators are already visible. Serious HELOC delinquency ticked up from Q1 to Q2 2025. The Federal Reserve Bank of New York reported that HELOC balances climbed to $434 billion by the end of 2025—up significantly from recent years—and that broader household delinquency is rising. Mortgage delinquencies overall reached 3.99% in Q3 2025, with MBA economists noting the role of a softer labor market and increasing personal debt obligations as contributing stressors.

This is not a crisis, but the trajectory is not neutral. And the volume of new HELOCs being originated in this environment means the risk is compounding quietly.

.avif)

Direct-source verification offers a solution

Yet despite these shifting conditions, income verification in HELOC underwriting has remained largely unchanged. Many lenders have historically relied on self-stated income, credit scores, and debt-to-income ratios calculated from prior-year tax returns to assess repayment ability. Some lenders offer explicitly no-doc or stated-income HELOCs, requiring little to no income documentation at all.

In a stable employment environment, that approach was defensible. In this one, it leaves lenders with a fundamental blind spot. They're making credit decisions based on what a borrower was making at last year’s tax time, not what they make today.

Fortunately for lenders, there’s a practical solution: direct-source income and employment verification, which pulls borrower data directly from payroll systems in real time.

Direct-source income and employment verification eliminates the lag that puts lenders at risk. It tells a lender not just what a borrower earned, but what they earned last pay period, whether they're still employed, whether their hours have been cut, and whether their income is stable or declining.

These are not nice-to-have details. In this environment, they’re the foundation of a defensible underwriting decision.

The cost argument has it backwards

The pushback I hear most often when I raise this topic is about cost. Incorporating direct-source income verification into HELOC underwriting is more expensive than relying on traditional methods like The Work Number (TWN) or a simple self-stated income check. That's true.

But the cost conversation is being framed wrong.

The question isn't whether verification costs money. The question is whether the cost of verification is higher or lower than the cost of default.

A borrower's FICO score doesn't change the morning after they're laid off. Their DTI ratio, as calculated from last year's tax return, doesn't capture the gig work that replaced their salaried income. And TWN can’t tell you if a borrower lost their job yesterday. When unemployment is rising, long-term joblessness is accelerating, and debt consolidation is driving origination volume, that lag becomes a liability.

What this means for lenders

I spent years in the mortgage business before joining Argyle, and I understand the pressure lenders are under to move fast, reduce friction, and compete on speed-to-approval. Those pressures are real. But originating volume is only valuable if the portfolio performs.

The lenders who will look back on this HELOC cycle with satisfaction will be the ones who recognized that the risk environment had changed and adjusted their verification practices accordingly. They won't be the ones using underwriting criteria built for a different era.

At Argyle, we make direct-source income and employment verification a reality for lenders. That means fresher data, faster decisions, and a clearer picture of actual repayment capacity—not a picture that's 90 days stale at the time of closing.

The HELOC market is growing, but the borrowers on the other side of these transactions are navigating a labor market that looks meaningfully different than it did just two years ago. They deserve underwriting that reflects that reality. So do the lenders extending them credit.

The cost of getting this wrong isn't a line item in a vendor budget. It's a portfolio problem waiting to happen. Contact our team at Argyle to learn how direct-source income and employment verifications can shield you from risk during the HELOC boom.

John Hardesty is SVP of Revenue at Argyle, where he leads the company’s go-to-market strategy for financial services. He previously served as GM of Argyle’s mortgage business line. You can connect with him on LinkedIn.