What Would a Recession Mean for Loan Fraud & Delinquency Risks?

Why lenders can’t afford to delay verification upgrades in 2025

As whispers of a 2025 recession grow louder—spurred by macroeconomic tensions, rising import tariffs, and persistent inflation—lenders face the question: What happens to loan fraud and delinquency risks if the economy turns?

Argyle’s The State of Income and Employment Verifications 2025 report highlights already concerning trends in fraud and delinquency rates across lending categories. And if historical precedent offers any indication, a recession would only exaggerate these trends. But there are steps lenders can take to mitigate risks even as factors affecting the economic outlook remain beyond their control.

This post examines how macroeconomic pressures amplify fraud and delinquency and why implementing direct-source verification processes early in the application funnel becomes even more critical during economic downturns.

The current fraud and delinquency landscape

Before exploring potential recession impacts, let's understand where we stand today. According to The State of Income and Employment Verifications 2025, the lending industry is already contending with troubling fraud and delinquency indicators:

- CoreLogic's Mortgage Application Fraud Risk Index was up 8.3% in 2024.

- The mortgage delinquency rate reached 3.98% in Q4 2024, up 10 basis points year-over-year.

- Credit card write-offs totaled $46 billion during the first three quarters of 2024, representing a 14-year high and a 50% year-over-year increase.

- Consumer loan delinquencies continued to climb from pandemic-era lows, affecting 2.73% of loans at U.S. commercial banks as of Q3 2024.

These statistics aren't occurring in a vacuum. They're influenced by several macroeconomic factors that would intensify during a recession:

- Persistent inflationary pressures

- Lower personal savings rates

- Increasing consumer debt levels

- Rising debt-to-income ratios

Learn more about the high fraud and delinquency risks lenders currently face. Download your free report. →

How recessions have historically impacted fraud and delinquency rates

Looking at previous economic downturns provides insight into what lenders might expect should a recession occur in the near future. Research from the Association of Certified Fraud Examiners (ACFE) found that the Great Recession of 2007 to 2009 led to an increase in fraud. According to the results of a survey published by the ACFE in 2009, 55.4% of fraud examiners reported that fraud had increased in the previous 12 months compared to prior years.

Fraud also increased during the recession and subsequent economic downturn associated with the Covid-19 pandemic. The Federal Trade Commission, for instance, found that consumer fraud reports surged during the pandemic, with estimated consumer losses climbing to $3.3 billion in 2020—nearly double the $1.8 billion reported in 2019.

Because economic recessions often lead to higher unemployment and reduced household incomes, it’s also harder for borrowers to keep up with loan payments. This directly contributes to higher delinquency rates. Lenders’ tendency to tighten lending standards during downturns can also restrict borrowers' ability to refinance or restructure debt, further increasing delinquency, especially among riskier borrowers.

During the Great Recession, for example, delinquencies increased significantly. Missed mortgage payments, in particular, closely tracked the rise in unemployment, demonstrating a clear pro-cyclical relationship between economic downturns and missed debt payments.

It’s worth noting that the Covid-19 pandemic actually led to lower delinquency and default rates, but that is largely attributed to a massive influx of government assistance in the form of loan forbearance programs and stimulus funds. If a recession comes to pass in 2025, lenders and borrowers should not necessarily expect comparable levels of government support.

Deteriorating economic conditions as a fraud motivator

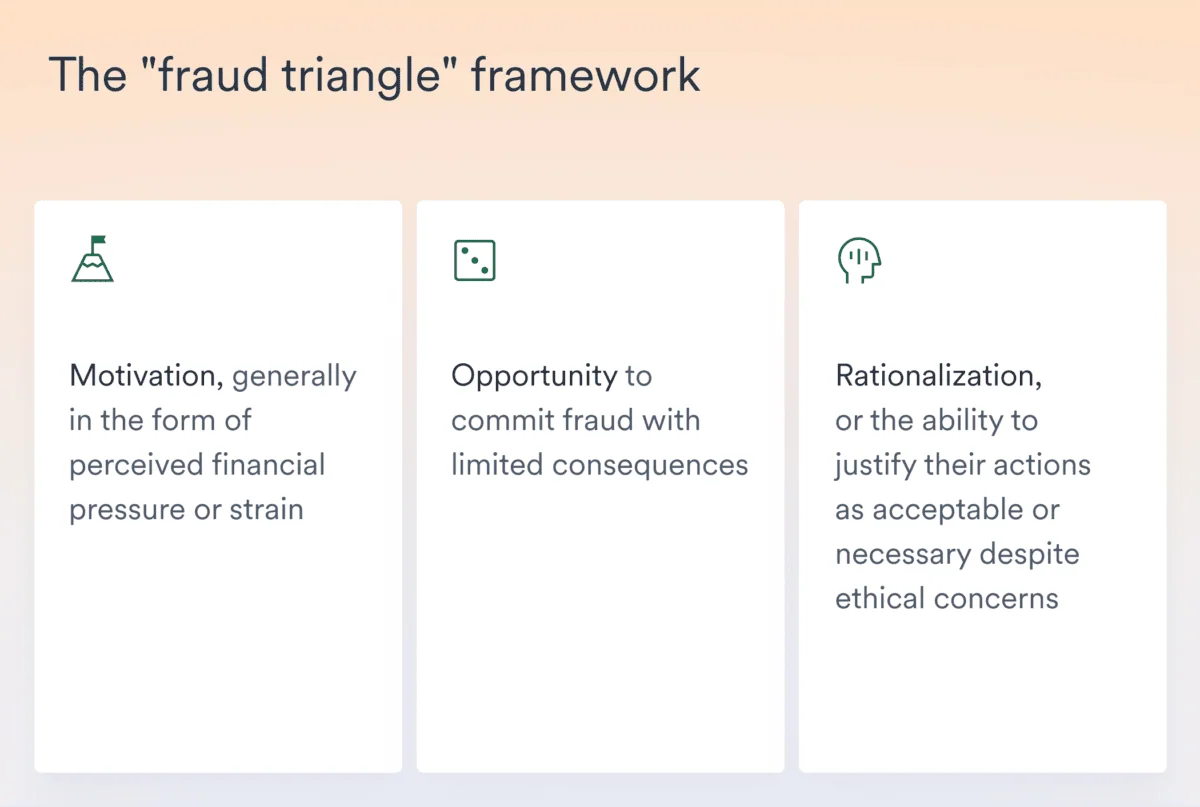

The correlation between economic downturn and rising rates of financial fraud makes sense. When forecasting circumstances that increase fraud risk, experts often reference the "fraud triangle" framework, which identifies three elements that typically converge before fraud occurs:

- Motivation, generally in the form of perceived financial pressure or strain

- Opportunity to commit fraud with limited consequences

- Rationalization, or the ability to justify their actions as acceptable or necessary despite ethical concerns.

These three factors working together create environments where fraud is significantly more probable. Unsurprisingly, the financial stress individuals experience during recessions intensifies the pressure component, making them more likely to commit fraud. It may also make rationalization easier, since they may believe that committing fraud is justifiable if it means helping themselves or their family get through a financially trying time that is beyond their control.

Meanwhile, today’s fraudsters may also have more opportunity to commit fraud given the rise in AI technology and fraud-as-a-service resources. As reported in The State of Income and Employment Verifications 2025, digital document forgeries were up 244% in 2024, and 512% more paystub templates were in circulation, suggesting both higher demand to inflate income on loan applications and easier access to the technology required to do so. And with 90% of document fraud signals invisible to the human eye, document manipulations are hard to detect. Lenders that rely on manual verification processes face substantial risk exposure.

Why early, digital VOIE is lenders’ best defense

In today’s high-risk lending environment, speed and accuracy are non-negotiable. Lenders need to identify bad actors fast—and that means verifying income and employment directly from the source and early:

- Move VOIE to the top of the funnel.

Most lenders wait until loan processing or underwriting to verify income and employment. But embedding verification in your POS at the point of application weeds out fraudulent and otherwise nonviable borrowers before they eat up your team’s time and resources. And because direct-source VOIE services like Argyle are 80% less expensive than verification databases like The Work Number, it’s no longer cost-prohibitive to verify at the top of the funnel. - Eliminate manual processes.

Paystubs, W-2s, and 1099s are increasingly easy to forge and counterfeit. By replacing manual uploads and reviews with direct connections to consumers’ payroll accounts, where income documents can be retrieved and digitally verified from the source of truth, lenders remove the opportunity for income fraud and substantially lower their risk.

Learn more about reducing loan fraud and delinquencies in a high-risk environment. Download your free report. →

Don’t wait for a downturn to hit

By the time recession headlines appear, fraud and delinquency risks will already be baked into your pipeline. Lenders who digitize and front-load their verification processes today will be better equipped to weather tomorrow’s economic storm.

Argyle, the leading provider of direct-source, consumer-permissioned income and employment verifications, makes it fast and easy to gain secure and reliable access to the most complete real-time datasets stored in consumers’ payroll accounts. With Argyle, lenders automate verification workflows to save time, reduce fraud and compliance risks, lower costs, and build better product experiences.

Reach out to our team to learn more about Argyle and how we can help reduce your risk in any lending environment.