American Pacific Mortgage cuts loan cycles by 12.5 days, saves over $1.5 million a year with Argyle

Branch-driven innovation turns consumer verifications into a competitive advantage

With more than 300 branch offices and more than 1000 mortgage originators across the country, American Pacific Mortgage (APM) is one of the nation’s largest and most successful independent mortgage banks. Its model gives branches autonomy to make decisions that best serve customers, while corporate leadership provides the technology, training, compliance and resources that help branches thrive. That continuous feedback loop between the field and corporate leadership proved critical when a growing challenge started affecting both manufacturing costs and customer experience.

Challenge

When Chris Sutherland, APM’s Director of Production Strategy, began hearing from branch managers that verification costs were exploding, he took their concern seriously.

“We take our marching orders from the field,” he says. “What do our branches need to be successful in this market, and how can we make them look good?”

The price hikes from legacy vendors were hitting branch P&Ls hard, and Branch Managers wanted to know if there was anything corporate could do to help. Multiple document requests were also frustrating customers and slowing down closings.

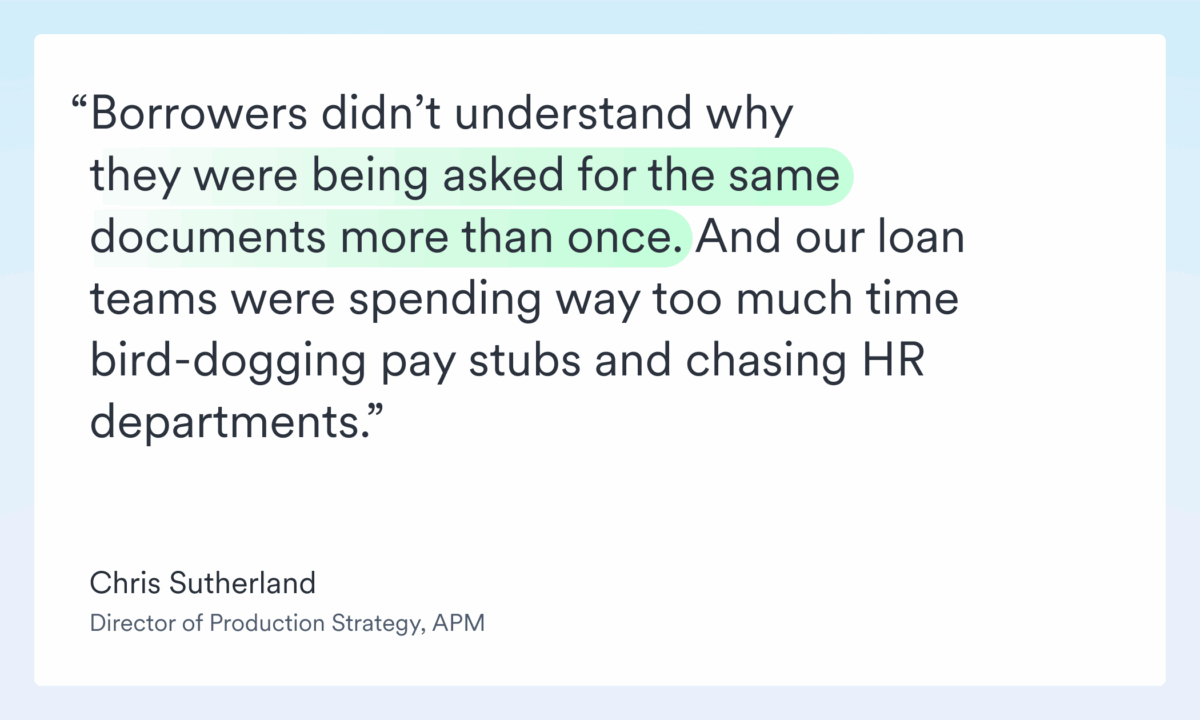

“Borrowers didn’t understand why they were being asked for the same documents more than once,” Sutherland recalls. “And our loan teams were spending way too much time bird-dogging pay stubs and chasing HR departments.”

Solution

APM needed an alternative to legacy verification services that could cut costs and improve customer experience without disrupting established branch workflows.

That search led to Argyle, a consumer-permissioned platform that connects directly to payroll and banking systems — unlike costly legacy providers that rely on static databases or document uploads — to deliver real-time, consumer-permissioned, GSE-eligible data.

When Sutherland’s team began evaluating Argyle, some initial hesitation centered on credentialed access and whether customers would feel comfortable logging in through a third party. Once customers understood that Argyle’s model works much like open authentication — the secure pass-through technology behind “Log in with Google” or “Log in with Facebook” — the concern disappeared. Customers never hand over passwords to APM or Argyle; they log in directly with their payroll or financial provider to authorize access, which they can revoke at any time.

That sense of transparency and control resonated with APM’s culture of trust.

“We vet a ton of technology,” Sutherland explains. “It seems like there’s a new LOS, POS or verification service every day. What stands out to us isn’t just the product, it’s the people behind it. One of the first things we evaluate when considering any new partner is their competence and trust level.”

APM first implemented Argyle within its loan origination system, the Encompass® LOS from ICE Mortgage Technology, giving loan officers instant access to verified income and employment data. But adoption was limited; relying on loan teams to trigger verifications later in the process still required manual coordination with customers.

Embedding Argyle at the point of sale (POS) solved that problem. By moving verification to the very start of the customer journey in nCino Mortgage, APM made it an effortless step in the application flow. Borrowers connect to their payroll providers in real time, and verified data moves automatically from POS to LOS, eliminating duplicate uploads and the manual follow-up loan teams once needed.

To validate the new approach, APM piloted Argyle with a cohort of innovative, high-producing teams known for giving candid feedback and influencing their peers. The pilot lasted just two-and-a-half weeks.

“For the first time ever, we spent under three weeks in pilot and already saw the savings,” Sutherland says. “So we made the call: we’re rolling this out for everyone. If a branch didn’t want it, they’d have to email us to opt out.”

That approach flipped APM’s usual deployment model. Instead of branches volunteering to opt in, Argyle was turned on by default across the organization.

“It was a bold move,” Sutherland says, “but once we turned Argyle on in nCino by default, orders absolutely hockey-sticked — and so did the results.”

Outcome

APM’s Argyle rollout has been a runaway success, delivering faster cycle times, major cost savings and a dramatically improved customer experience.

- 12.5 days faster from start to funding

With Argyle, APM no longer waits for employers to return calls or for customers to send in pay stubs. Loans with Argyle verifications close more than 12 days faster, including a 20% reduction in the processing-to-underwriting milestone.

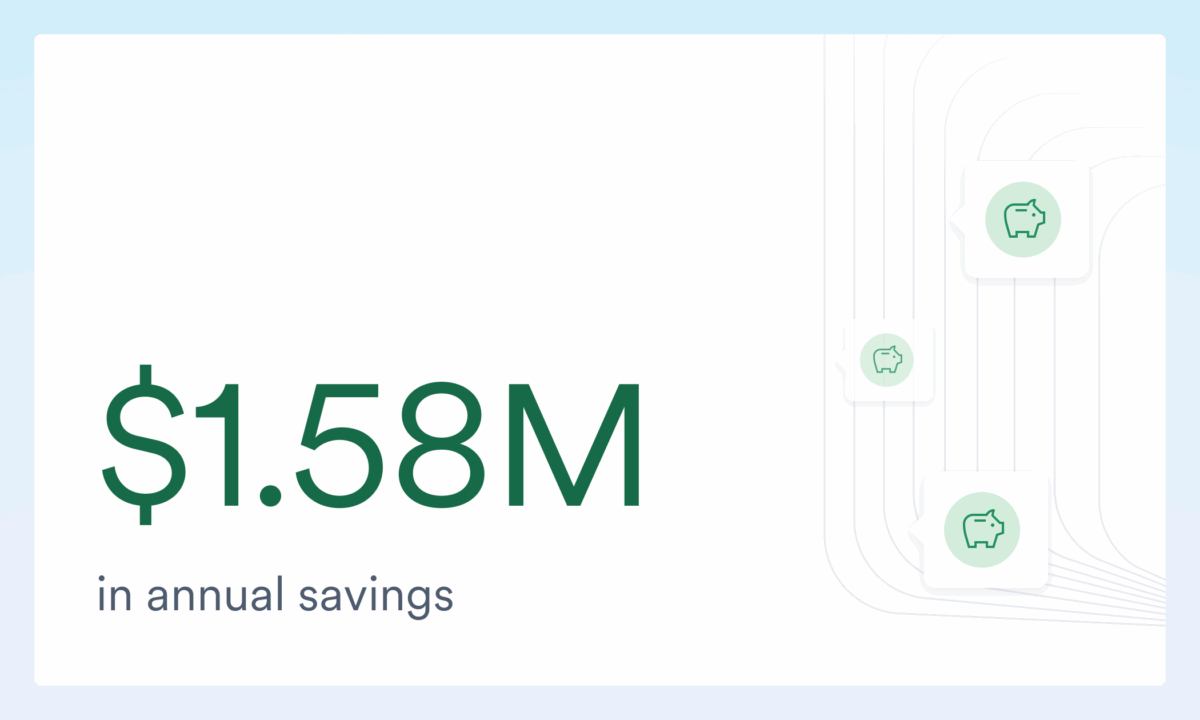

“The reduction in cycle time blew my mind,” says Sutherland. “Every day saved matters — not just for us, but for borrowers eager to close.” - $1.58M in annual savings

Branch-level concerns that moving verifications to the POS could drive up costs have proven unfounded. In just five months, APM saved $700,000 in verification expenses, putting it on pace to save more than $1.58 million annually — a clear win for branch-level profitability.

“We just had to get the branches comfortable with the math,” Sutherland says. “Moving verifications to the point of sale may mean more verification orders overall, but Argyle is so much more cost-effective than legacy providers that the savings are obvious.” - Higher conversion rates and better customer experiences

Embedding Argyle at the point of sale lets customers verify income and employment within their normal application flow, a change that has meaningfully increased verification success rates.”

“Once we made it part of the natural flow, completion rates skyrocketed,” says Sutherland. “You no longer have processors sending links or explaining what to do — it just happens as part of the application.”

- More R&W relief and stronger GSE partnerships

Argyle’s GSE-accepted data has helped APM receive rep and warranty relief on more loans, which has only strengthened the lender’s relationships with Fannie Mae and Freddie Mac.

“Our agency representatives are patting us on the back,” Sutherland says. “They love seeing lenders embrace technology that strengthens loan quality and lending efficiency.” - Exceptional responsiveness from the Argyle Team

APM credits Argyle’s partnership and customer success team as key drivers of adoption and performance.

“We give Argyle a lot of kudos for how responsive they have been,” says Sutherland. “They listen, and in several cases they have blown our hair back with how quickly they’ve responded to and executed on requests. Argyle has been a great partner for APM, and that’s what moves the needle.”

By embedding Argyle directly into its LOS and POS ecosystems, APM turned one of the most cumbersome steps in the mortgage process into a competitive edge.

To learn more, check out Argyle’s webinar recording with APM and ICE Mortgage Technology titled “Powering the Modern Loan Process.”