Mortgage Automation: 6 Ways Manual Verifications Are Holding Lenders Back

Research shows most mortgage lenders still spend valuable time and resources on manual VOIE processes—but Argyle’s direct-source data is helping to change that.

Despite ongoing digital advancements, certain aspects of mortgage lending remain largely analog. Chief among them is verification of income and employment (VOIE).

According to the latest research from Stifel, 50% to 75% of mortgage lenders (or the third-party vendors they partner with) still rely on manual verification processes. These include collecting paystubs and other documents from borrowers, processing their data by hand, and painstakingly identifying and correcting any oversights until a loan is finally closed.

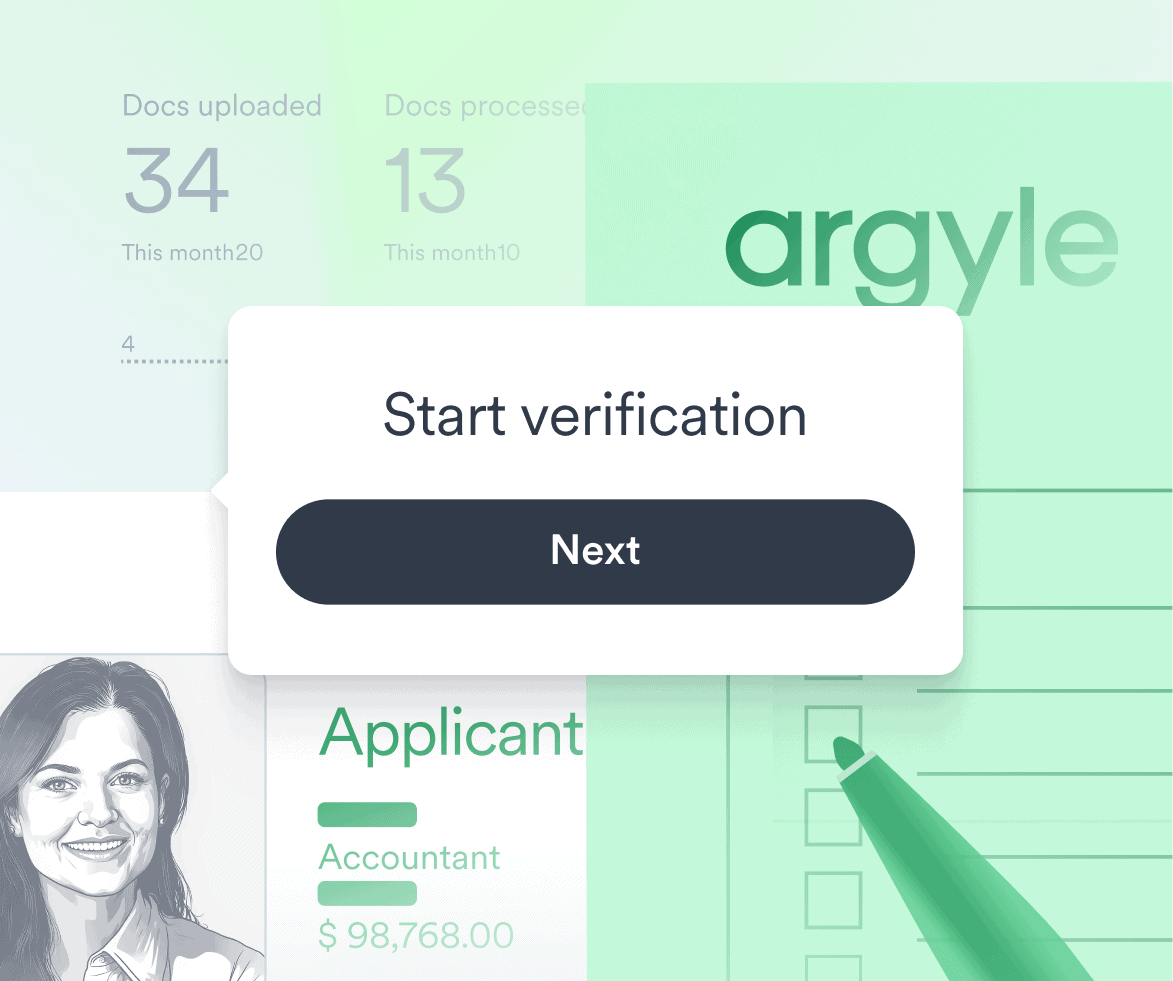

That’s why solutions like Argyle—which connect lenders to real-time data, pulled directly from borrowers’ payroll accounts—have emerged to automate VOIE from end to end.

Below, we list six fundamental challenges lenders face with manual verification processes—and six ways that direct-source data providers like Argyle can resolve them.

1. It takes days or even weeks to verify borrowers.

Manual income and employment verifications typically involve several time-consuming steps. Loan officers don’t just have to chase down borrowers to collect essential documents like paystubs and W-2s; they also have to contact borrowers’ current (and possibly former) employers to confirm their source(s) of income.

All told, these steps can take quite some time to complete, especially if the employers in question are too busy or too difficult to track down. Recording and organizing information by hand also means there’s ample opportunity for error, with one misstep threatening to restart the process.

Meanwhile, loan applications sit idle—frustrating borrowers and impeding lenders’ ability to grow their business.

By contrast, Argyle grants lenders instant and ongoing access to borrowers’ income and employment data by tapping directly into their payroll records.

Lake Michigan Credit Union (LMCU) estimates that, before partnering with Argyle, it would take their team an average of three weeks to manually verify a borrower’s income or employment. With Argyle, it’s done in under a minute.

2. Profits are drained by high operational costs.

Lenders often pay steep prices to buy VOIE reports from databases like The Work Number (TWN), only to then have to collect documents like paystubs anyway and fill in any incomplete fields.

Between high labor expenses, lost revenue from delayed loan approvals, and mounting costs with each reverification, these legacy processes can take a substantial hit on a lender’s bottom line.

Subscribing to Argyle not only cuts down on inefficiency, it unlocks continuous access to data and documentation as well as regular refreshes and change alerts—so lenders can get all the information they need, when they need it, at no extra cost.

In just their first year with Argyle, for instance, NFM Lending saved 80% on income and employment verifications, reducing the cost of every loan by around $100. And they expect to save even more year over year, as adoption increases across their team.

3. Data quality is compromised by avoidable errors.

Even the most talented humans inevitably make mistakes, especially when workloads are high and deadlines are tight. Details can easily get lost or muddled when data entry is carried out by hand, whether information is being transferred from a physical document or transcribed from a call.

In turn, flawed data can lead lenders to misunderstand their borrowers, make unsound loan decisions, and expose their businesses to risk and loss.

One study found that the defect rate for mortgages has been growing dramatically across loan types, with income and employment data leading all defect categories with a share of over 37%. Luckily, Argyle’s clean data helps confront this issue.

Because Argyle pulls data straight from the source of truth (i.e., a borrower’s payroll account), there’s no opportunity for error. The VOIE report a lender receives is a one-to-one representation of what’s in their records.

It’s what allows Argyle partners like AmeriSave to keep more accurate loan files and reduce their buyback risk when selling to GSEs.

“Argyle delivers every data field required by the GSEs more than 95% of the time, and because of that, they really shine in getting rep and warrant relief for the lender. About one-fifth of loan files that contain an Argyle VOIE report are deemed eligible for rep and warrant relief, which is much higher than we’ve seen from other verification providers.” – Magesh Sarma, Chief Information and Strategy Officer at AmeriSave

4. Reports are often missing required information.

When collected manually, income and employment data only includes the fields that are readily available (and easily attainable) on a borrower’s paystubs and W-2s—or offered up by an employer.

That information may not be comprehensive enough to satisfy a lender’s rigorous underwriting criteria. Even if it is, it may not be presented in a convenient, accessible format that lenders can quickly interpret and plug into their underwriting model.

Argyle returns all of a lender’s required VOIE data 95% of the time. That includes granular, gross-income details like bonuses, commissions, and deductions, all organized in an intuitive, standardized format.

Argyle’s partners at Delta Community Credit Union receive complete VOIE reports for over 60% of their members. That means they can limit the number of applications they route to more expensive, less efficient manual methods further down their waterfall, saving them countless hours and resources.

5. Unreliable data increases rates of delinquency and fraud.

Data that’s incorrect, incomplete, or outdated opens a lender to risk and loss. That could be at the hands of (intentional) wrongdoing or due to (unintentional) loan defaults, if loan decisions don’t reflect what borrowers can actually afford.

This is an especially urgent issue, considering that rates of both fraud and delinquency are generally on the rise.

Argyle offers uninterrupted access to borrowers’ income and employment data, with continuous monitoring and real-time alerts whenever there’s a significant change. That means lenders can be proactive when it comes to reducing the risk of default.

Since there’s no middleware, and data flows straight from a borrower’s payroll account, Argyle’s VOIE reports are also tamper-proof.

Kathy Weber, Delta Community’s vice president of residential lending, shared that the integrity of Argyle’s data has allowed Delta to feel more confident during the verification process.

6. Busywork leads to a poor borrower experience.

Finally, asking borrowers to track down and submit financial documents—and potentially resubmit updated versions prior to closing—can quickly strain lending relationships.

Too much upfront friction can even cause borrowers to churn during the application process. According to one McKinsey study, only 42% to 67% of borrowers report being happy with their mortgage process, with the top complaint being a poor origination and onboarding experience. For these borrowers, having an exceptional mortgage experience was almost as critical as securing the best possible rate.

Argyle’s automated VOIE makes it easy for borrowers to share their income and employment data with a click (leading to an impressive 55%+ conversion rate). Plus, Argyle’s consumer-permissioned process puts borrowers in control of their own personal information.

According to the LMCU team, Argyle not only optimized their member experience, but also saved their members time and money in the process.

“Our primary goal is always to provide our members with high-quality financial services. By increasing the speed of verifications and passing our savings down to them, we are able to offer our members the best possible mortgage experience, without time-consuming blocks or extra fees.” – John Harpst, Vice President, Community Lending at Lake Michigan Credit Union

Get faster, simpler verifications with Argyle.

You can learn more about our best-in-class Income & Employment Verification solution or our work in the mortgage industry on our website—or reach out to our team to set up a demo.