Lenders look to verification waterfalls to keep loans flowing

Mortgage lenders are increasingly adopting verification waterfalls into their loan origination processes to streamline data flows and maximize conversion rates.

The mortgage industry has undergone a dramatic shift in the way lenders approach income, employment, and asset verifications. Processes that once relied heavily on manual workflows and legacy databases now leverage more sophisticated, automated methods with built-in fallback strategies to optimize results.

Known as verification “waterfalls,” these strategies integrate a range of data sources—including direct payroll connections, direct banking connections, and document processing—to create seamless borrower experiences while driving down processing time and costs.

Historically, building such waterfalls meant contracting with multiple verification providers, each specializing in different data sources and methods. Today, however, top providers offer a range of verification solutions as part of a comprehensive platform. That means lenders can maintain the same breadth of verification options while simplifying their provider management.

This evolution has been spurred by both the limitations of traditional methods and the emergence of consumer-permissioned, direct-source data solutions that consistently deliver higher conversion rates, faster close times, and lower costs. Better still, forward-thinking lenders can integrate some of these methods directly into the point-of-sale (POS) and loan origination systems (LOS) they already use, instantly transforming their workflows without disrupting their existing tech stacks.

Here’s what you need to know about this growing technology trend.

What’s a verification waterfall?

For those unfamiliar, a waterfall is any multi-step workflow where steps follow a linear sequence, progressing from one to the next in a pre-defined order—much like water flowing downstream in a fixed direction.

In the context of mortgage loans specifically, it refers to a recent practice where increasing numbers of lenders are using multiple data sources to complete their verifications instead of relying on a single method. They often put their strongest, most valuable data source at the top of the waterfall and move to the next method in the sequence if the first data source is unsuccessful or insufficient.

A change in course

Everyone agrees that manual, labor-intensive verification processes—like calling up borrowers’ employers or collecting and reviewing their documents by hand—should be a last resort. Typically, these tasks incur high operational costs that reduce profitability and eventually get passed down to borrowers in the form of tacked-on fees. Moreover, phone calls and paper chases can extend loan processing times by days or weeks, delaying approvals and increasing rates of application abandonment.

That’s why, for nearly 30 years, lenders have attempted to automate verifications using any means possible. Until recently, this involved relying on borrower data purchased from databases like The Work Number (TWN)—usually without borrowers’ knowledge or explicit consent. This data often turned out to be incomplete, inaccurate, or outdated, having sat static in a repository for months.

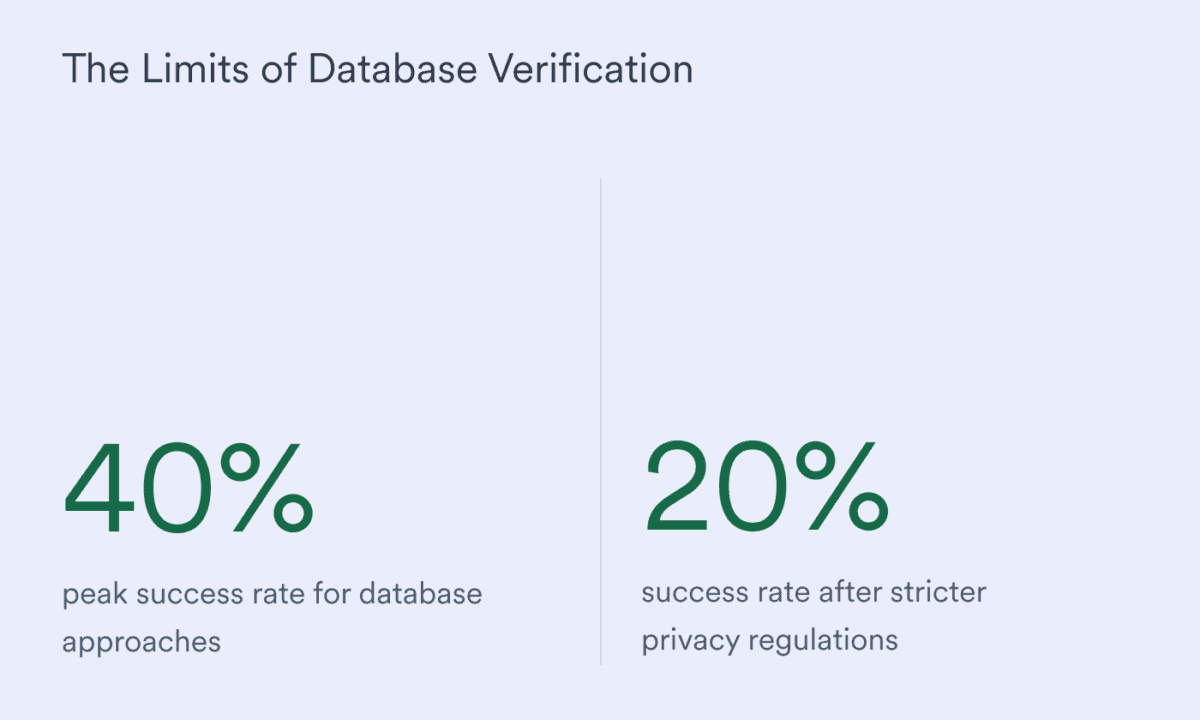

Even at its peak, database approaches only achieved success rates of around 40%—and now that data privacy regulations are making it easier for consumers to restrict the unauthorized resale of their personal data, conversions have dropped closer to 20%. As a result, lenders relying mainly on databases end up having to manually verify a vast majority of their applicants.

Despite waning effectiveness and high price tags, many lenders continue to turn to databases for verifications—a phenomenon that’s done nothing to curb runaway net production losses. But now, thanks to the emergence of new verification methods, there are more automation options than ever before.

The modern verification landscape

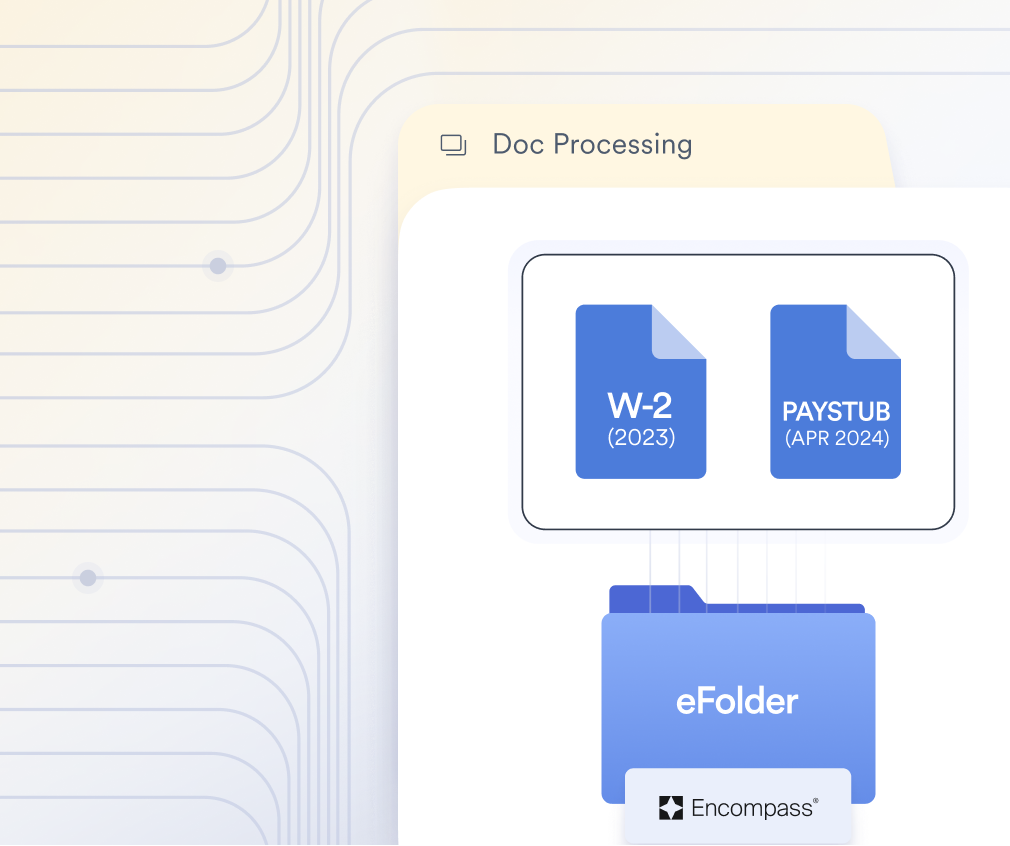

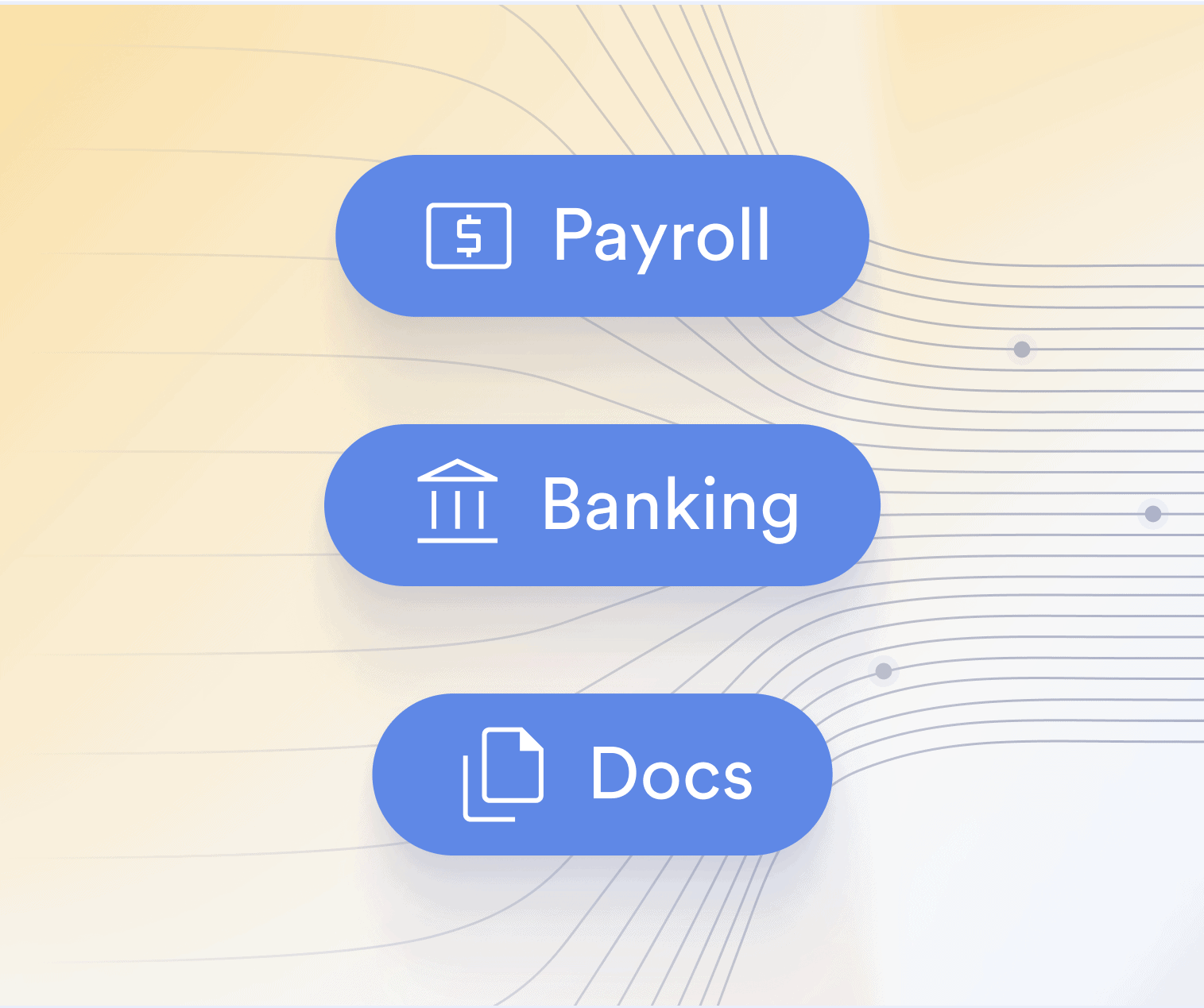

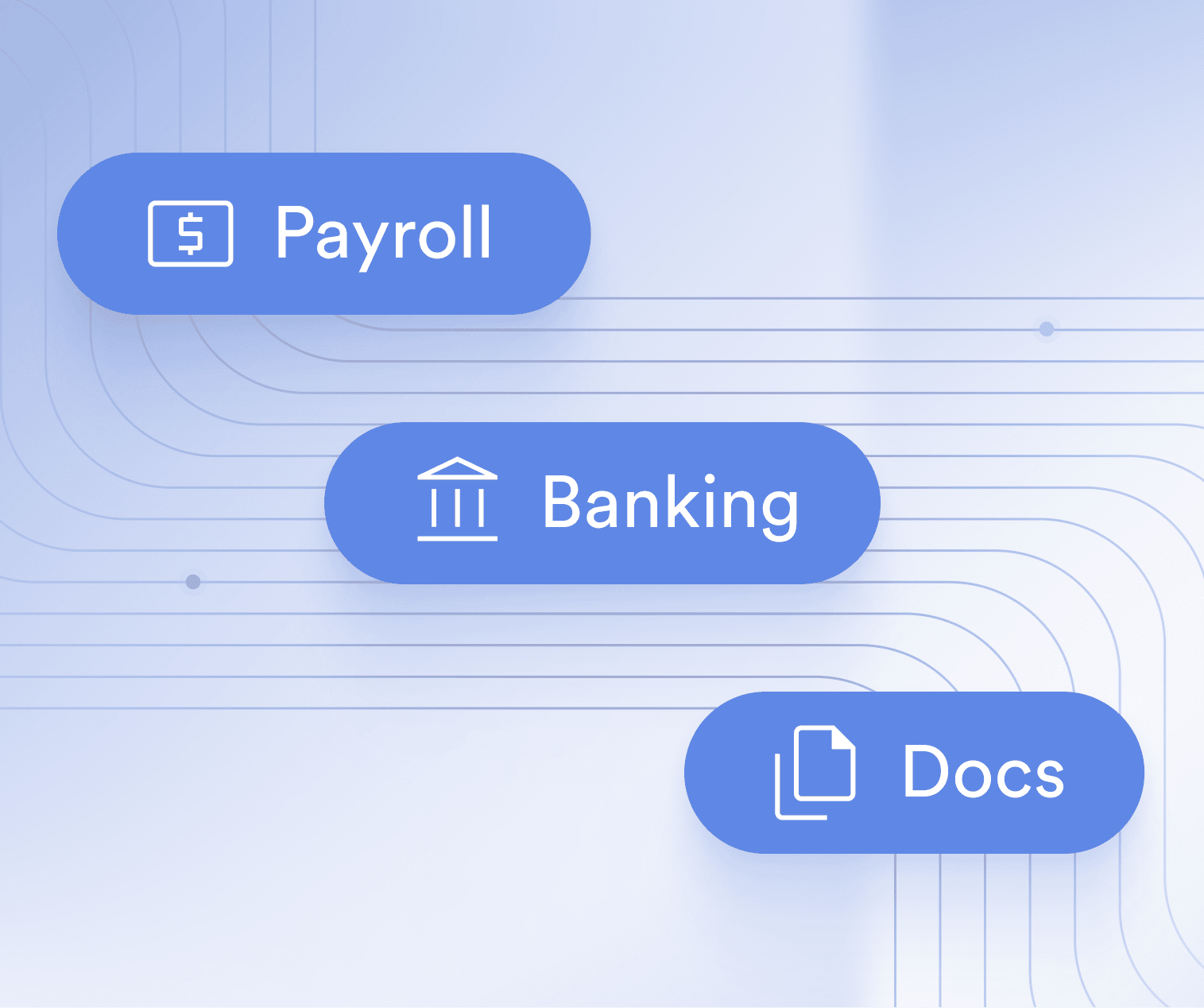

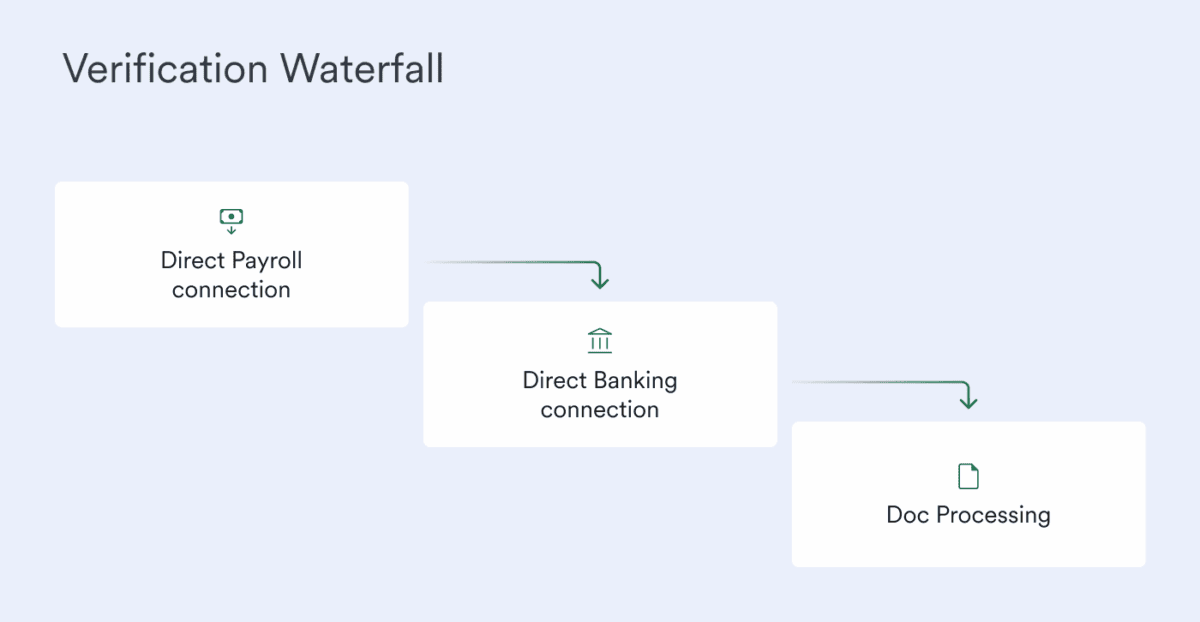

Today’s tech ecosystem offers multiple pathways for mortgage lenders looking to automate their income, employment, and asset verifications. They can use direct payroll connections to verify income and employment through platforms that connect directly to borrowers’ employer and payroll provider accounts. They can use direct banking connections to verify assets and infer income from deposit histories pulled straight from borrowers’ bank accounts. And they can use OCR-powered document processing solutions to automatically extract data from uploaded documents like paystubs, W-2s, and 1099s.

The real breakthrough comes when lenders combine these verification options into a comprehensive waterfall—maximizing the relative strengths of each data source while unlocking broader coverage across applicant types and income streams.

The case for verification waterfalls

By incorporating multiple data sources and verification methods into their workflows, lenders prevent applications from grinding to a halt when one solution is unsuccessful. Instead of being relegated to a loan processor’s manual verification queue—where applications might languish for days or weeks—borrower information is simply passed down to the next designated solution in the waterfall until a successful verification is achieved. Since this process requires no human intervention and limits the need for back-and-forth with borrowers and their employers, it leads to significant time and cost savings, not to mention a better borrower experience.

Moreover, some verification providers offer all three methods (income, employment, and asset verifications), reducing the need to contract, get support from, and pay for multiple providers for one step in the loan origination process.

Building an effective waterfall strategy

Whether integrating a verification waterfall with an existing POS or LOS or building a standalone solution, a lender must decide which data sources to include and in what order.

The strongest approach generally follows this sequence:

1. Direct payroll connections: Lenders can streamline income and employment verifications through direct, real-time connections to a borrower’s employer or payroll provider account, pulling granular income and employment details straight from the system of record.

2. Direct banking connection: Lenders can connect directly to a borrower’s bank account to verify their assets, calculate any supplemental income streams, and paint a more complete picture of their financial health.

3. Document processing: Lenders can automatically process uploaded financial documents like paystubs, W-2s, and 1099s as a final attempt before resorting to manual review.

This structure maximizes the potential for automation—and captures the greatest number of conversions—while ensuring every applicant has multiple pathways to complete their verification.

Direct payroll connections often sit at the top of the verification waterfall as a preferred method due to their strong performance. Argyle’s direct payroll solution, for instance, sees 55% conversion rates, 90% data completeness, and cost savings up to 80% compared to other sources.

A lender might be tempted to put the lowest-cost method at the top of their waterfall by default—but there are other important factors to consider beyond the price tag. For instance, an independent mortgage bank that sells a large portion of its loans to Fannie Mae and Freddie Mac would want to prioritize a verification method and provider that qualifies for GSE-authorized relief from representations and warranties.

Additionally, many lenders are discovering significant cost advantages by moving their verification processes earlier in the workflow to the POS stage, where having GSE-compliant verifications from day one can amplify savings and reduce buyback risk.

Timing the verification waterfall in the mortgage process

In fact, the most effective verification waterfalls operate early in the loan application process, within the POS system—fully embedded in the Form 1003 application flow.

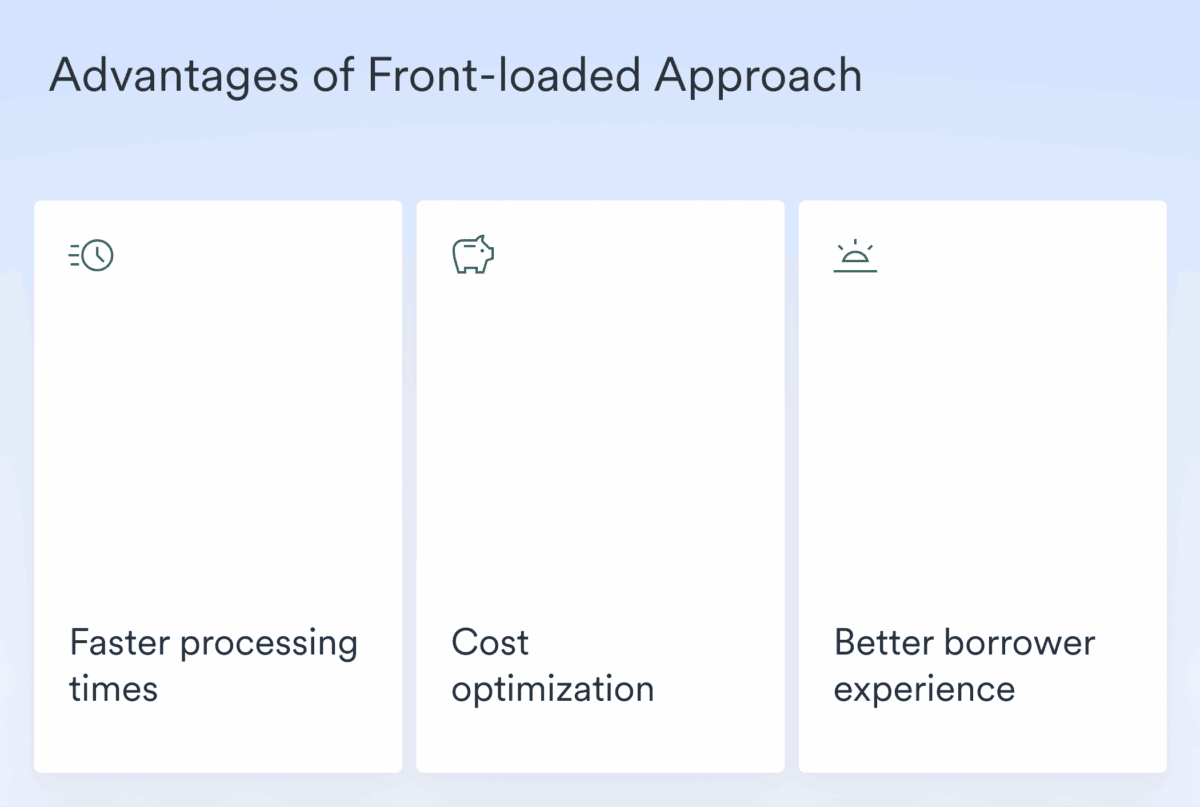

This front-loaded approach creates a smooth, digital-first workflow that increases pull-through rates and reduces friction, delivering several immediate advantages:

- Faster processing times: Qualifying borrowers in real time and early in the application process—rather than days or weeks later—improves the overall cycle time.

- Cost optimization: Implementing verifications at the POS actually proves more cost-effective than waiting until later stages in the process.

- Better borrower experience: Streamlined verification processes reduce back-and-forth paper chases that frustrate borrowers and cause them to abandon their applications.

The benefits of moving verifications to the POS can be substantial. For example, Homestead Funding—a family-run, multi-state licensed mortgage lender—initially saw solid savings of $2K to $6K per month by incorporating Argyle’s verification solution into their LOS. But when they moved Argyle up to the POS stage, their monthly savings tripled to approximately $15K.

For independent mortgage banks like Homestead that sell the majority of their loans, starting with GSE-compliant verifications provides maximum opportunity for relief from reps and warranties while ensuring every loan is ready for sale from the outset.

The bottom line

Regardless of how a verification waterfall is configured and placed, its core value remains the same: reducing manual verification volumes while increasing conversion rates and data quality.

In short, the verification waterfall isn’t just a trend—it’s an essential strategy for lenders looking to compete in today’s fast-paced, crowded mortgage market. By strategically implementing multiple data sources in a carefully coordinated sequence, lenders can maximize automation, reduce their overall costs, and deliver the seamless experience that today’s borrowers demand.

Ready to see how a verification waterfall can transform your lending operations?

Reach out to Argyle’s team to learn more about our industry-leading verification platform—which combines direct-source payroll connections, direct-source banking data, and OCR-powered document processing into a single, comprehensive solution.