Keep users engaged with solutions unlocked by employment data and payroll connectivity

Creating a long-lasting relationship with a large network of users is the ultimate goal for neobanks. Once you have onboard a user, what are you doing to retain them and encourage engagement? Neobank users can be fickle and quick to switch if a competitor can offer them a desirable banking solution.

Our data shows, user payroll connectivity unlocks as much as $38 of revenue opportunities per month for a neobank, depending on the services a user takes advantage of. That’s money out the door if users are just engaged with your checking account offering.

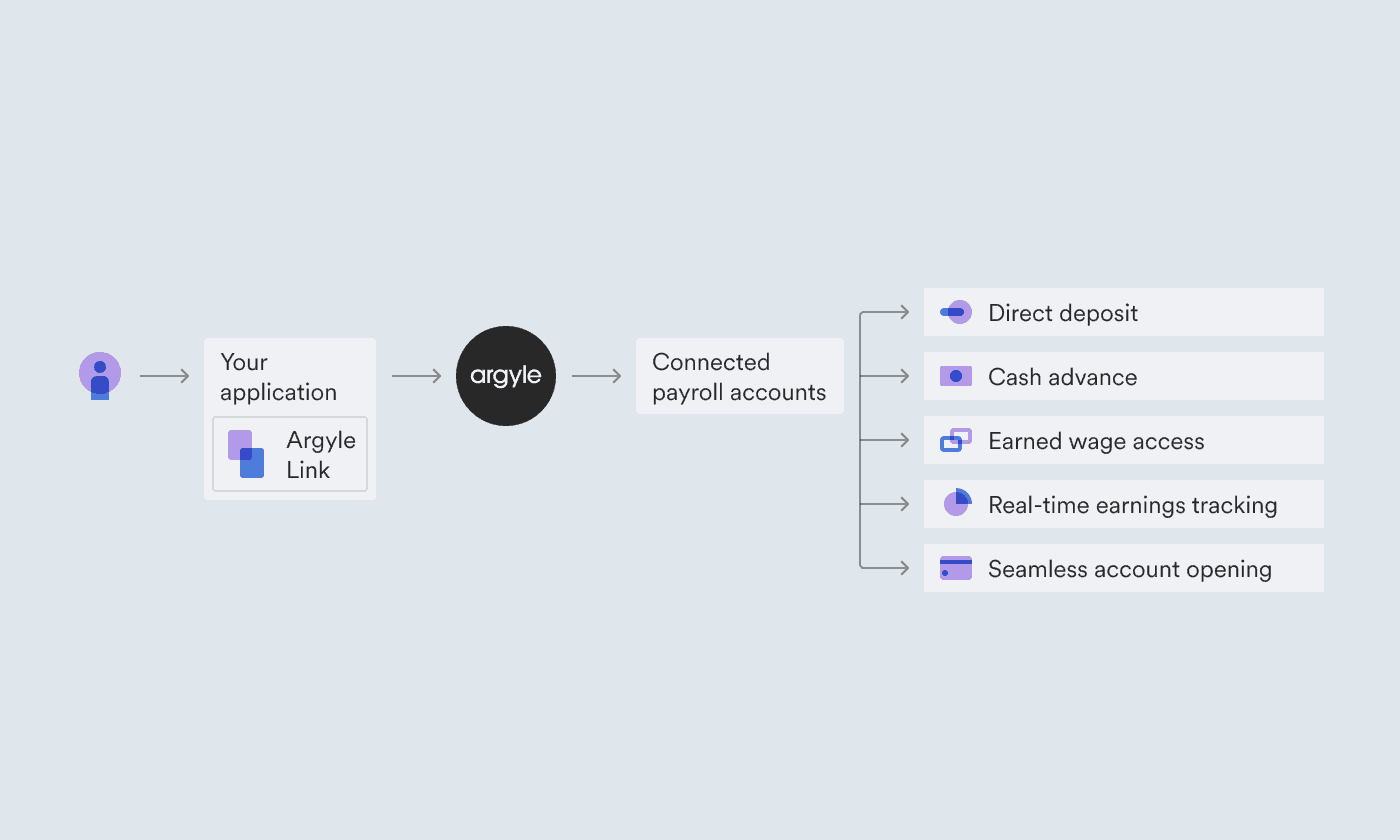

Let’s take a closer look at the products you can offer with the help of a robust employment data platform.

1. Direct deposit acquisition

Increasing assets under management as a user’s primary bank

Becoming your user’s primary account means a significant uptick in user activity, ultimately leading to an increase in managed assets, product adoption, and revenue. However, direct deposit switching can be cumbersome for both the bank and user, requiring too much coordination—not to mention paperwork—between you, your users, and their employers or payroll providers.

With Argyle, users find their employer or payroll provider in Argyle Link, log in using their payroll credentials, and confirm their direct deposit switch — it’s that simple. You can also monitor users’ deposit activity over time and receive notifications if users switch deposits away from your neobank so you can reach out to learn more.

Expected returns: $10/month per account

Based on industry data and client results, neobanks can expect up to $10 a month in interchange revenue from active users who have set up direct deposit, depending on size of deposits. Adding more assets under management also unlocks the possibility of offering additional solutions for users, and this can be validating in a crowded market.

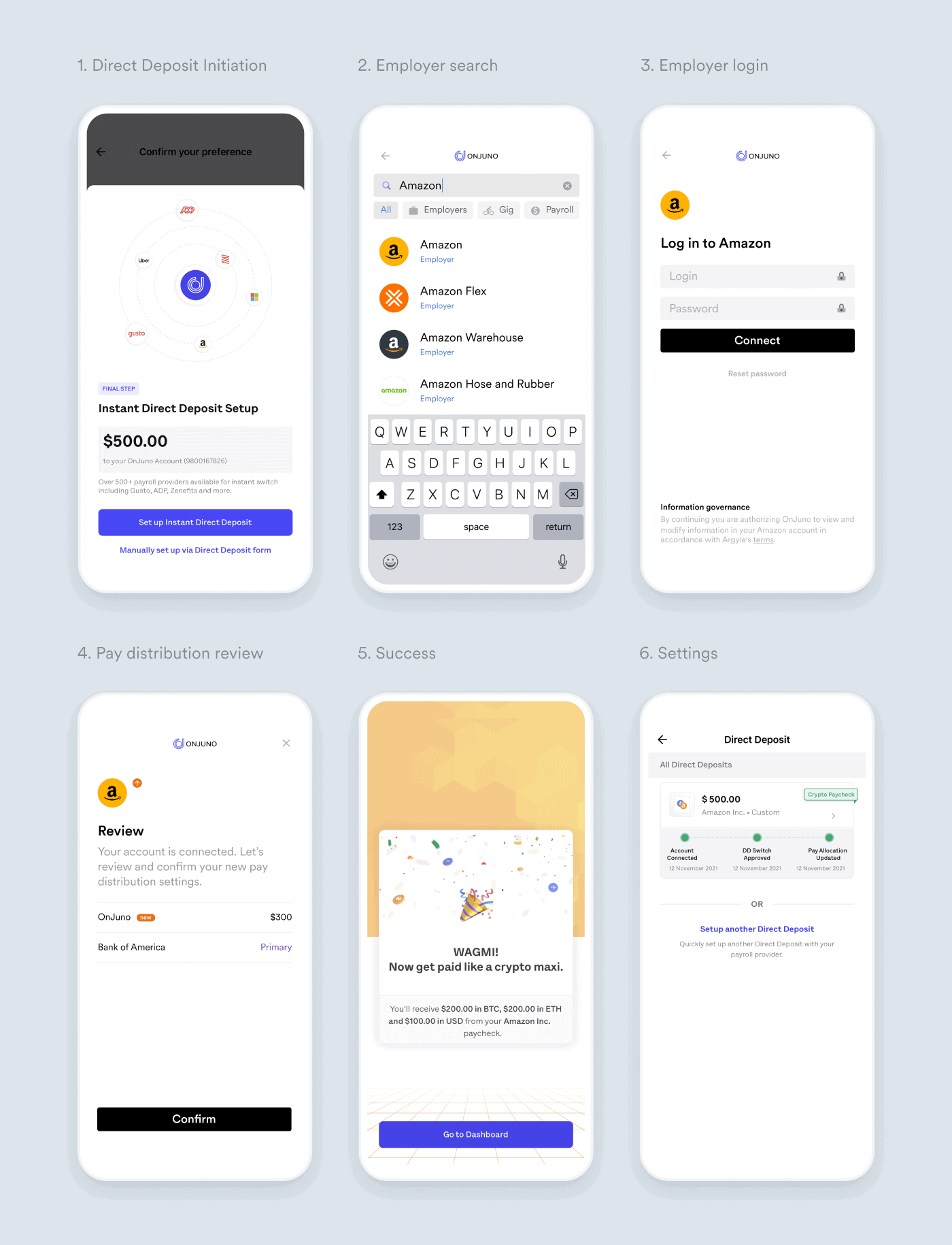

OnJuno improved its conversion rate 30x with Argyle

OnJuno offers high-yield checking accounts, including the option to set up a direct deposit and receive part of your cash paycheck in crypto in any wallet of your choice. After months of working with another direct deposit provider, the company leaders knew it needed a new partner with a higher level of customer service and better user experience. That’s when they found Argyle.

Argyle now sits within the OnJuno app when a user sets up an account, and when a user decides to allocate a percentage of their salary to be paid in crypto currency through OnJuno.

“Having access to Argyle’s direct deposit APIs ensures that more users deposit their salaries into OnJuno, which takes us closer to the goal of converting OnJuno to a primary banking account for our users,” said Associate Product Manager, Ankit Pandey.

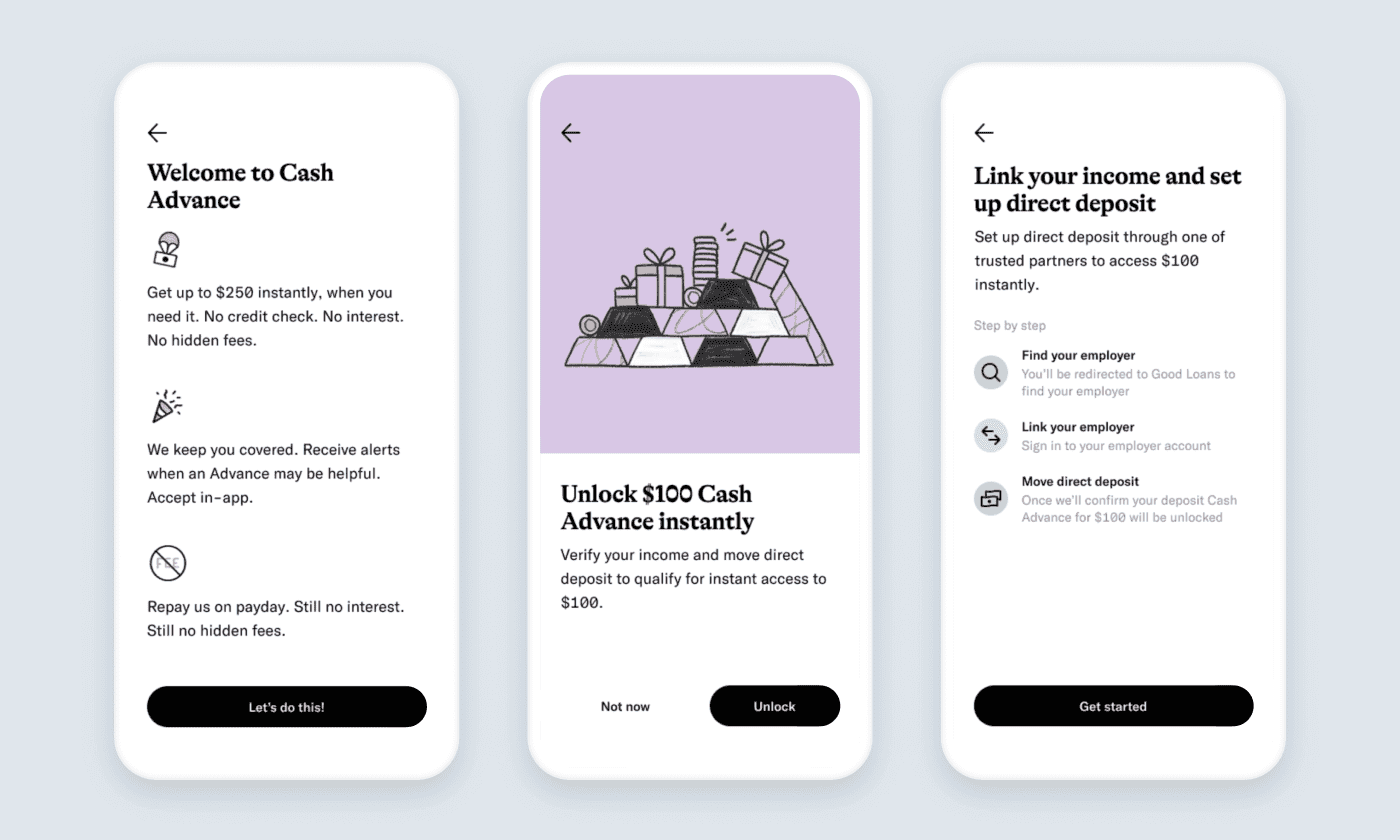

2. Cash advance

The modern solution to outdated payday loans

Allowing users to withdraw money before it is available in their checking account is a risk if you don’t know your user very well. With Argyle’s income and employment data, you don’t have to guess when the next paycheck will hit their account, or how much it will be.

Expected returns: $5/month per account

Neobanks can expect up to $5 a month in revenue from active users who have set up cash advances. Argyle’s real-time employment and income data can streamline the cost of underwriting even further.

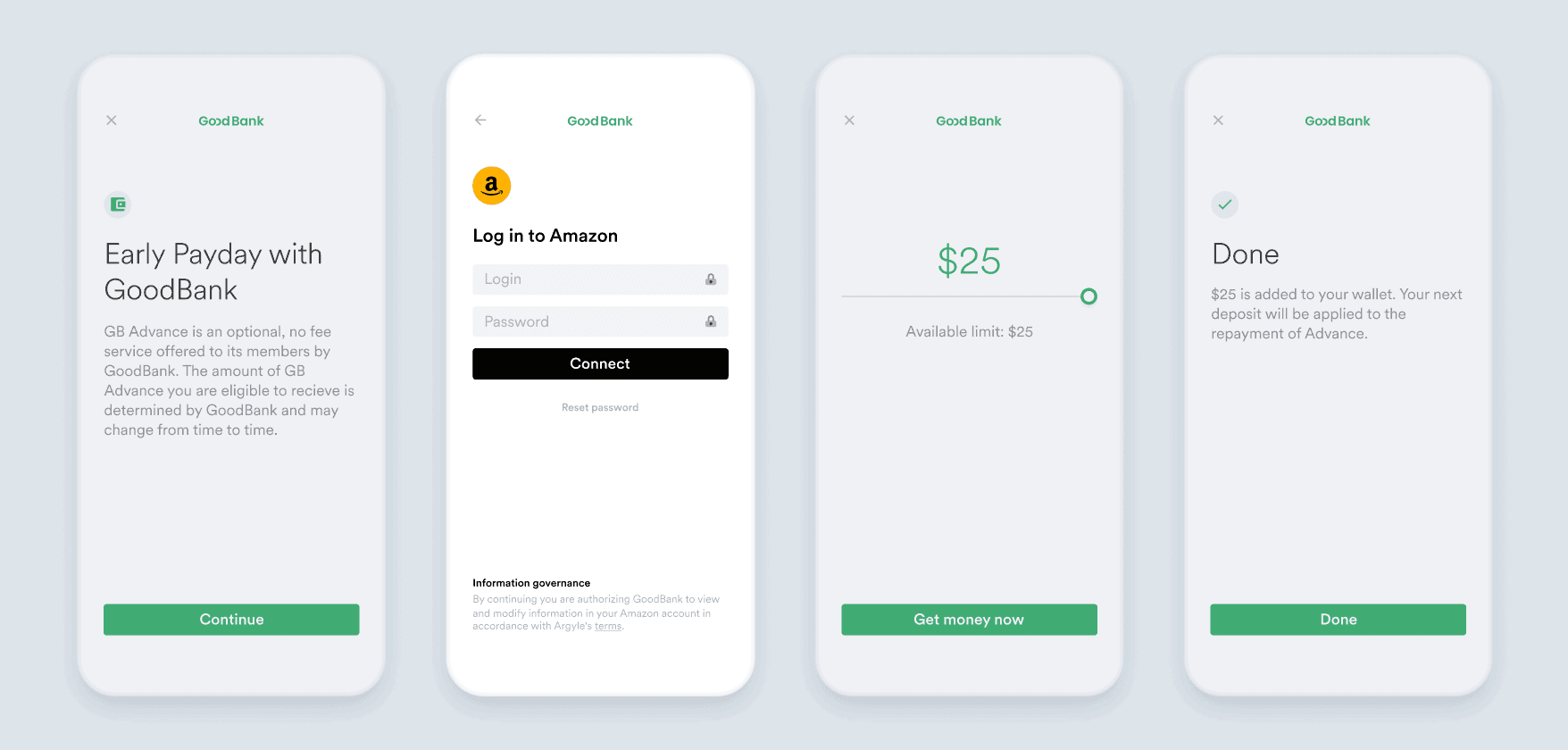

Empower uses Argyle’s data for smarter underwriting

Empower uses Argyle to not only connect accounts for direct deposit switching, but also underwrite users looking for a cash advance. By evaluating data endpoints like hire date, employment status, and income (gross and net pay), the company can be confident in offering a cash advance and can offer users up to $250 immediately. No waiting on a direct deposit to hit their Empower account necessary.

3. Earned wage access

No salary guesswork required

Offering users the ability to access the money they’ve earned before their scheduled payday is only possible when you know in real time how much a user has worked. On-demand pay is quickly becoming a valuable payroll feature for workers, but most employers are not equipped to make this shift.

Neobanks have the opportunity to step in and meet the demand of these workers, and gain loyal customers in the process.

In addition, offering early access to wages your users have already earned, with constant, real-time updates on hourly shift data and work records limits the risk to both your bank and the user of default.

$6/month per account

Neobanks can expect up to $6 a month in revenue from active users who have set up earned wage access. As employers struggle to find ways to provide this highly sought after benefit, neobanks have the ability to move fast and address that demand within a user’s checking account.

Lend with confidence

Using Argyle’s comprehensive payroll data, lenders have greater visibility into each client, enabling them to approve requests quickly and confidently. It also empowers lenders to offer lower, more competitive rates in a crowded marketplace, as you have additional information about the user filling in the blanks.

4. Real-time earnings tracking

Offer an engaging banking experience

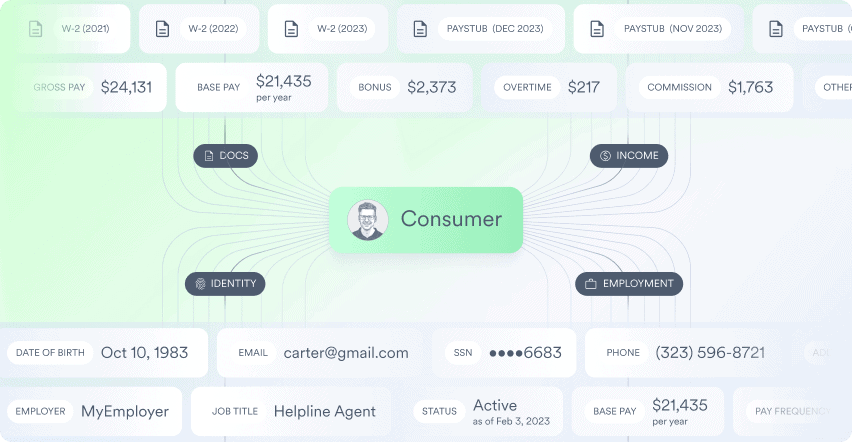

Argyle’s verification of income and employment is not a one time snapshot of your users, but a continuous data pipeline you can reference as frequently as needed. This feature allows neobanks like yours to not only verify a user’s income, but also monitor significant shifts. Our webhook notifications alert a customer right away if a user’s status changes, like if they’re laid off or receive a raise.

Users spend most of their time on tracking and repayment screens

App Annie found that users are spending 45% more time on finance apps year over year, meaning the financial uncertainty of the last year has translated into highly engaged banking customers. Finding a financial partner who not only supports their banking needs, but can help users plan for the future and be proactive is a key differentiating factor.

Many banks offering income tracking find their users spend the majority of their time on those screens. Including a calculator that helps users plan how much they could earn in the coming months makes you a key player in their financial planning efforts. The more involved your bank is in their goals, the more likely they are to make your bank their primary checking account.

5. Seamless account opening

No one likes to repeat themselves, and often getting started with a new bank is a series of FAQs the user has seen hundreds of times before. For existing users you can pull from data the user has already included, but what about new users? With Argyle, you can skip the basic questions with pre-populated information from a user’s payroll account.

This not only saves the user time, but saves you time as well, since the information has already been verified. By using user-permissioned and verified data you can fast track your bank account verification process. Quick and frictionless account openings help you start the client relationship off on the right foot.

Argyle helps Moves automate account openings

Moves had originally only come to Argyle to support income verification, but quickly embraced additional solutions like direct deposit switching and seamless account opening.

“It became obvious that the next layer of problems to solve involved banking infrastructure to help workers manage all of their earnings and cash flow in one place,” said Matt Spoke, CEO and Founder of Moves Financial. “With Argyle, it’s all automated, so users don’t have to go through multiple sources and manually transfer information.”

The value of user stickiness

Becoming your users’ primary bank account requires not just meeting their checking account needs, but building additional products to keep users in your environment. Offering competitive products is dependent on knowing your client and having confidence in your user’s income and employment story.

Expected returns: $1-15/month per account

Beyond the earnings specific to products offered, neobanks can expect between $1 to $15 a month in revenue from active users, just for continuing to keep their checking account open.

The impact of the additional products real-time employment data unlocks

Argyle combines functionalities that other platforms tend to in silos. With real-time, continuous access to employment and payroll data, neobanks can establish more meaningful relationships with their users and offer more tailored financial services.

Having access to a user’s income and employment data unlocks the lending capabilities and niche banking products that delight users and keep them loyal to your brand. It can even unlock user segments you might have dismissed before due to incomplete data.

Reach out to your product manager to discuss our range of solutions or to set up a demo.

* Dollar value figures based on client feedback and sourcing from American Banker, JD Supra and Fortune Magazine.