Amidst rising consumer expectations, seamless digital experiences are becoming nonoptional—and mortgage lending is no exception.

From the borrower’s perspective, going through the mortgage loan process feels like navigating a complex maze, where they face hurdles at every corner. Each friction point in this highly competitive lending environment is a potential drop-off point, where the lender risks losing the applicant.

Research suggests that even slight friction in a lender’s digital processes can harm their relationships with borrowers, driving many to contemplate switching to a competitor. On the other hand, when done right, a seamless and positive mortgage loan experience can lead to higher conversions and increased borrower satisfaction.

That’s where Argyle shines. Our Income & Employment Verification solution for lenders is built to make the mortgage loan experience better for borrowers and lenders alike.

In this article, we’ll dive into some common challenges borrowers face in the mortgage loan process, the ways in which Argyle solves them, and how that benefits lenders by extension.

Challenge 1: Time-consuming applications and too much paperwork

Despite the shift to digital lending, the mortgage lending process remains significantly time-consuming for both borrowers and lenders.

To verify their financial health and satisfy lenders’ risk management and compliance protocols, borrowers must provide documentation like paystubs, employment letters, W-2s, and 1099s. For borrowers, meeting these requirements has typically involved tracking down these documents one by one, downloading or scanning them as PDFs, and sharing them with a loan officer—sometimes via unsecure pathways like email.

This approach not only lacks efficiency, it is also unreliable. Incorrect or insufficient documents or mistakes in the provided documents can cause unnecessary delays and even credit rejections, presenting one more obstacle for borrowers in already tightened lending conditions.

Furthermore, it forces borrowers to shoulder the burden of supplying income and employment data and documentation during verification and reverification, potentially causing drop-offs.

The Argyle Answer: Automate, Automate, Automate

Argyle fully automates verification of income (VOI) and verification of employment (VOE) processes, streamlining the application journey. This results in faster turnaround times, reduced friction, and a more efficient workflow for borrowers and lenders.

And when we say fully, we mean it. Not only does Argyle instantly generate VOI and VOE reports on demand, our technology also imports all required income and employment documentation in real time, straight from the source of truth: borrowers’ payroll accounts. That means no more paper shuffling or PDFs for borrowers, no risk of inaccurate or incomplete documentation, and far less admin for lenders.

Moreover, Argyle provides continuous access to these documents and data, so when lenders go to reverify income and employment at closing, they don’t incur additional costs. Because of these efficiencies, Argyle lowers verification costs by anywhere between 60% and 80% compared to Equifax’s The Work Number (TWN) and manual verifications.

Plus, lenders can rest easy knowing that they’re in compliance, as Argyle is an authorized report supplier for Fannie Mae’s Desktop Underwriter® validation service, a component of Day 1 Certainty®.

Challenge 2: Data security threats and breaches of trust

Innovative verification technologies like Argyle get confused with third-party data digital verification providers like TWN, but there are distinct differences.

Unlike Argyle, TWN is a static database of income and employment data that’s updated only semi-regularly via an outdated flat-file method.

In addition to carrying the risk of errors that can result in unjust credit denials and data breaches that can put their financial lives at risk, TWN and its lookalikes monetize consumers’ personal data without their fully informed consent. The truth of the matter is, employers and payroll providers sell their personal information to TWN for a hefty sum—a cost TWN passes onto lenders, which raises the costs of closing for borrowers. Together, these factors erode borrower trust.

“It’s mind-blowing. And people have no idea,” said Jon Weinberg, Wayne State University law professor, in an NBC article about TWN. “Equifax has not, historically, been real good about data security […] About making sure only the people who are supposed to see the information actually see it.”

The Argyle Answer: Total transparency and consumer-permissioned flows

Argyle lets borrowers control their data, offering a comfortable and trustworthy experience. With Argyle, borrowers link their payroll account at onboarding, granting lenders real-time access to their payroll records.

Additionally, safeguarding consumer data is top priority at Argyle, as our solution is fully certified for and compliant with SOC 2 Type 2 standards. SOC certification is indicative of the measures an organization takes to safeguard its customers’ sensitive data, as well as the data of its customers’ clients. And SOC 2 Type 2 certification is not only the most thorough one out there; it’s also the toughest to achieve.

This just goes to show that Argyle is built with data security in mind.

Challenge 3: Compromised conversions

Compared to legacy verification databases, next-generation direct-source verification solutions are the obvious answer. However, many direct-source providers mislead lenders by claiming conversions if a connection was made—even if they fail to successfully retrieve borrowers’ data. Too often, this leaves lenders without access to necessary information, and it leaves borrowers scrambling to gather their income and employment data and documentation the old-fashioned way.

The Argyle Answer: High coverage and conversion rates

This is where Argyle stands out. With a demonstrated, market-leading conversion rate of more than 50%, Argyle makes it remarkably easy for borrowers to establish a payroll connection to share their income and employment data, and we do it through conversion-optimization features like smart search, single sign-on (SSO) authentication methods, and in-app password reset flows.

But more than that, Argyle successfully returns more data than any other provider on the market, and we only count a connection as a conversion when the data is actually pulled through.

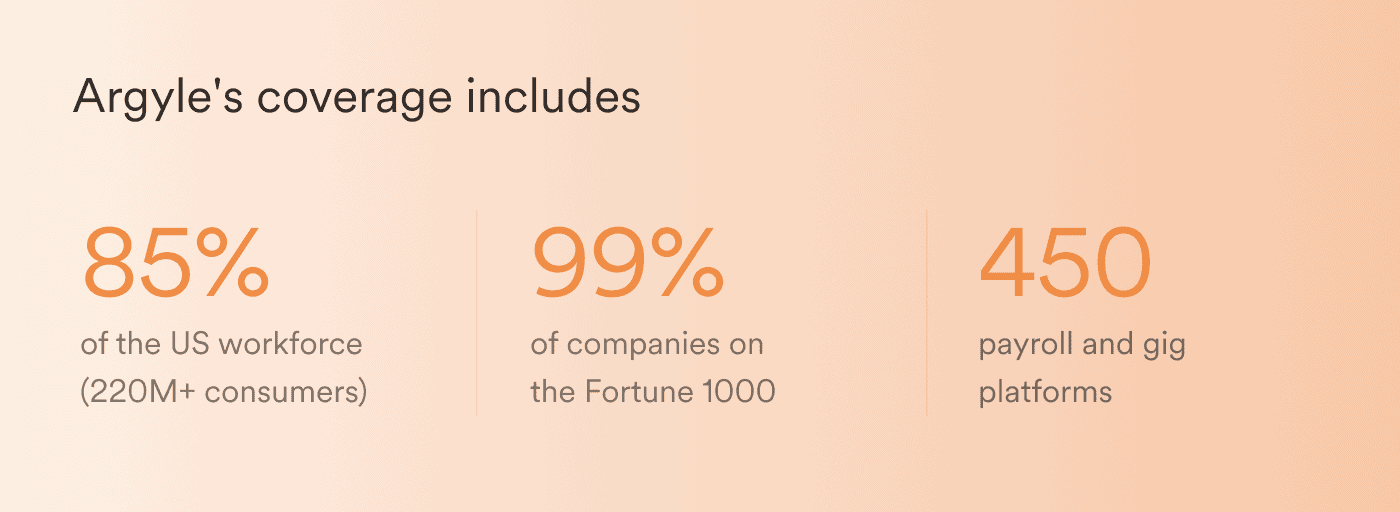

This is in addition to Argyle’s impressive total coverage, which includes:

85% of the US workforce (220M+ consumers)

99% of the Fortune 1000

450 payroll and gig platforms

Happy borrowers are better for business

In mortgage lending, borrower satisfaction has become non-negotiable, particularly in today’s fiercely competitive landscape. With loan origination being the first touchpoint for most borrowers, a seamless onboarding and application process makes all the difference in starting on the right note.

Moreover, satisfied borrowers tend to establish lasting relationships with their lender. So, reducing friction in the mortgage loan process can result in better Net Promoter Scores (NPS), more referrals, and opportunities to upsell or cross-sell services. Argyle transforms the mortgage loan experience while addressing borrowers’ pain points head-on. Contact us to see how Argyle can help you on your journey.