Even before getting money into a worker’s hands companies struggle to run payroll. Calculating hours, overtime, deductions, reimbursements and tax obligations is complex enough. That’s why, across all verticals, companies use a 3rd party payroll provider to manage the payment of their workers. The issue still remains — what’s the most efficient way to get money into the hands of workers?

The story makes enough logical sense: the first company to ever leverage what we know today as direct deposit (instead of checks or cash) was the United States Air Force in 1974. The pilots were in the air so handing or sending them checks did not do much to get their cash into their banks. The government needed a simpler and more reliable way to pay workers so they leveraged a middle man in the Federal Reserve. In association with NACHA (The National Automated Clearing House Association), the Air Force would send money through a newly created service named the ACH Network (or The Automated Clearing House Network) where the money would go from the Air Force to the Federal Reserve and then to each pilot’s bank account automatically.

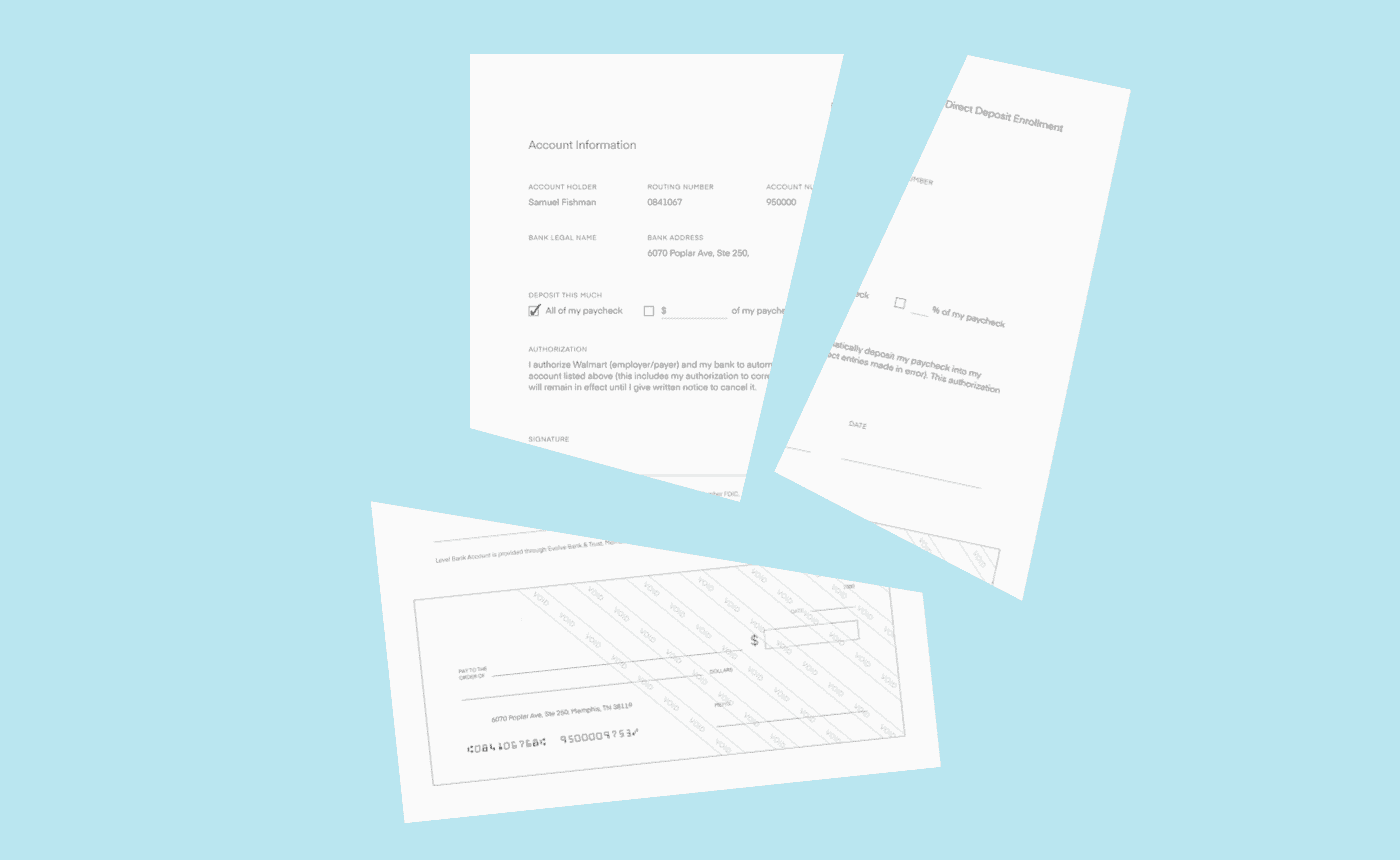

The problem — how do you know where each pilot banks? And this is where an unfortunate alternative storyline emerges that Argyle has fixed. But more on Argyle later. The solution at the time was to have banks generate a DDA, or Direct Deposit Authorization Form. (This is an example of one that Wells Fargo still uses today). This form looks complicated but it really boils down to getting the Air Force the unique routing and account number combination for each pilot. The bank generates the form, the pilot gives the form to the HR department at the Air Force, someone in the HR department of the Air Force types in the routing and account number for that pilot and the direct deposit system works. It was such a success that the second company to use the ACHN for direct deposit services was the social security administration for paying out retirement benefits.

What these paper DDA’s effectually do is trade one type of manual work for another. While, before, a company needed to cut checks and hand them out to workers, now workers need to get forms from their bank and hand them to the company they work for. Less work to manage payroll but more work for everyone else. The goal was to automate the entire payment process — NACHA fell short.

The storyline need not have gone this way. Banks could have worked with NACHA in a more future-forward way where routing and account information could be sent into a company’s payroll service by leveraging the ACH Network for their own benefit. And because workers do change banks and set up multiple accounts for different purposes we are left with a manual authorization process that is error-prone and make’s it quite hard for a worker to set up direct deposit.

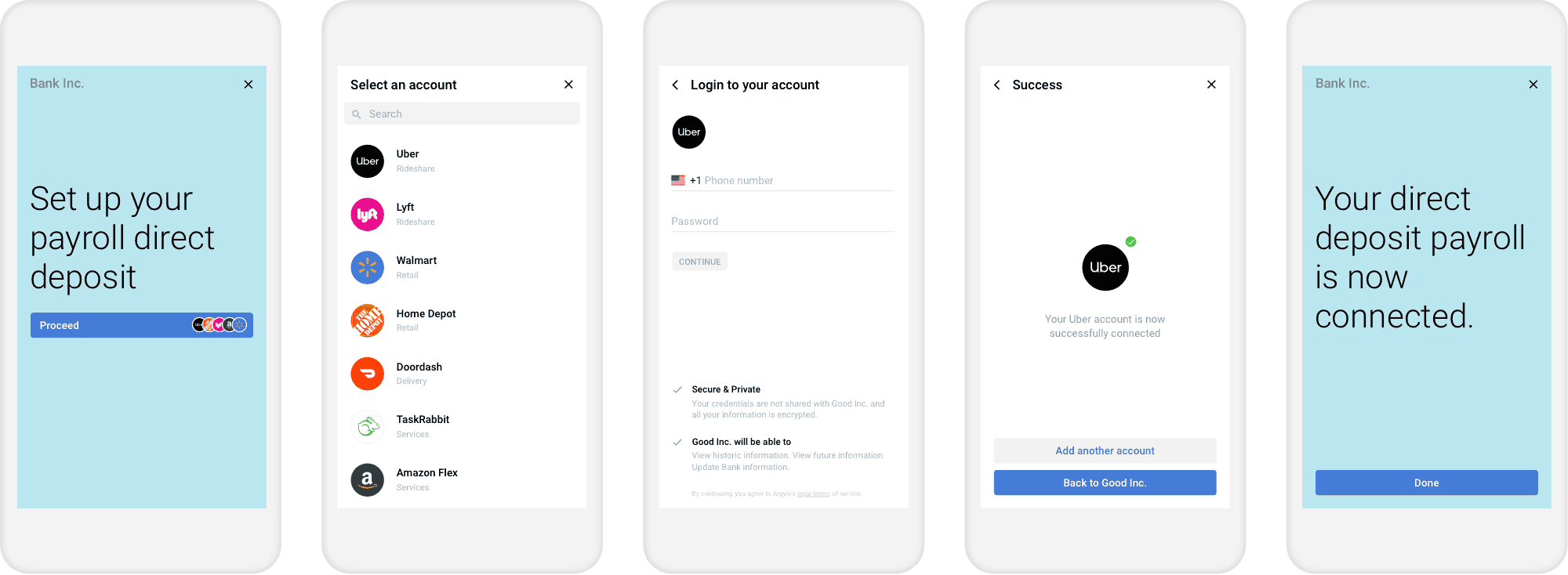

Argyle has fixed this and we call it Automated Direct Deposit Switching. The solution is simple enough — when a worker changes their bank, they are prompted to select what company (or companies) that pay them. Argyle then connects into each of the selected companies and update’s the routing and account numbers in that worker’s profile. Everyone wins. The bank no longer needs to generate a direct deposit authorization form, the worker no longer needs to deal with a form, and the HR department for a company does not need to process a form.

There are two notable firms that provide alternatives to these Direct Deposit forms.

Founded in 2014, ClickSwitch provides an on-premise-based system where financial institutions can direct ClickSwitch to change direct deposit information on their behalf through a portal. ClickSwitch works its magic by officiating the manual process away from the bank. They have a large phone bank in Minneapolis that calls on HR departs on a bank’s behalf, hundreds of fax machines that send direct deposit change forms, and a large mailing operation that sends direct deposit change forms to employees when all else fails. Less automation; more obfuscation. The largest drawback is that the process can take weeks to complete and neither the financial institution or the worker knows if ClickSwitch was successful until the next payroll run is completed.

Pinwheel is a new firm founded in 2020 in San Francisco. They should be commended for working through this process from an automation first approach and connecting directly with payroll vendors. The downside – payroll vendors do not control direct deposit information; companies do. As you look through the landscape of the largest companies who pay workers, they each have a custom implementation and process for running their payroll. Pinwheel might work for the 10 person bakery down the street – it will not work for Walmart.

Just like Equifax is smart to understand that income and employment verification is a feature, not a product, so too is Argyle. What both ClickSwitch and Pinwheel miss is that providing direct deposit switching is one of many features enabled by accessing a worker’s employment data itself. It’s access to the data set itself that enables services such as Income and Employment Verification, Real-Time Earnings Transparency, and yes, Automated Direct Deposit Switching. Why would a business want to have services like these from multiple vendors if one company can provide them everything through a single API?