Argyle’s real-time employment data unlocks affordable income-based loans and helps you get paid on time.

Featured contributor Geoff Brown, Cofounder & CEO of Highline

Access to credit is widely understood as an important tool to manage financial resources, provide a buffer for emergencies or shortfalls, and even support wealth-building. But, individuals or families that have had financial challenges in the past are often denied access to new credit because historical challenges reflect in their credit scores, making it even more difficult to rebuild their financial standing. Out of need, these individuals turn to any loans they can access, often from a limited set of high-cost options.

Particularly in short-term small-dollar credit, there is a shortage of non-predatory products for Americans that need access to cash to avoid penalties like overdraft or utility disconnect fees. This loan segment provides critical bridge funding, particularly for low-income populations, but lender expectation of high defaults results in a dearth of affordable products for the consumers that need them.

Enter paycheck-linked lending—a lower-cost option for consumers, enabled by a structural reduction in default risk resulting from Argyle’s new technology.

With paycheck-linked lending, loans are automatically repaid through preset distributions directly from a borrower’s paycheck, instantly reducing the risk of default. Paycheck-linked lenders experience 2/3 fewer defaults versus traditional ACH debits. This is game changing for both customers and lenders.

Let’s take a closer look at how these payroll deduction loans works, how it helps both lenders and borrowers, and how Argyle’s technology is making it possible.

How it works

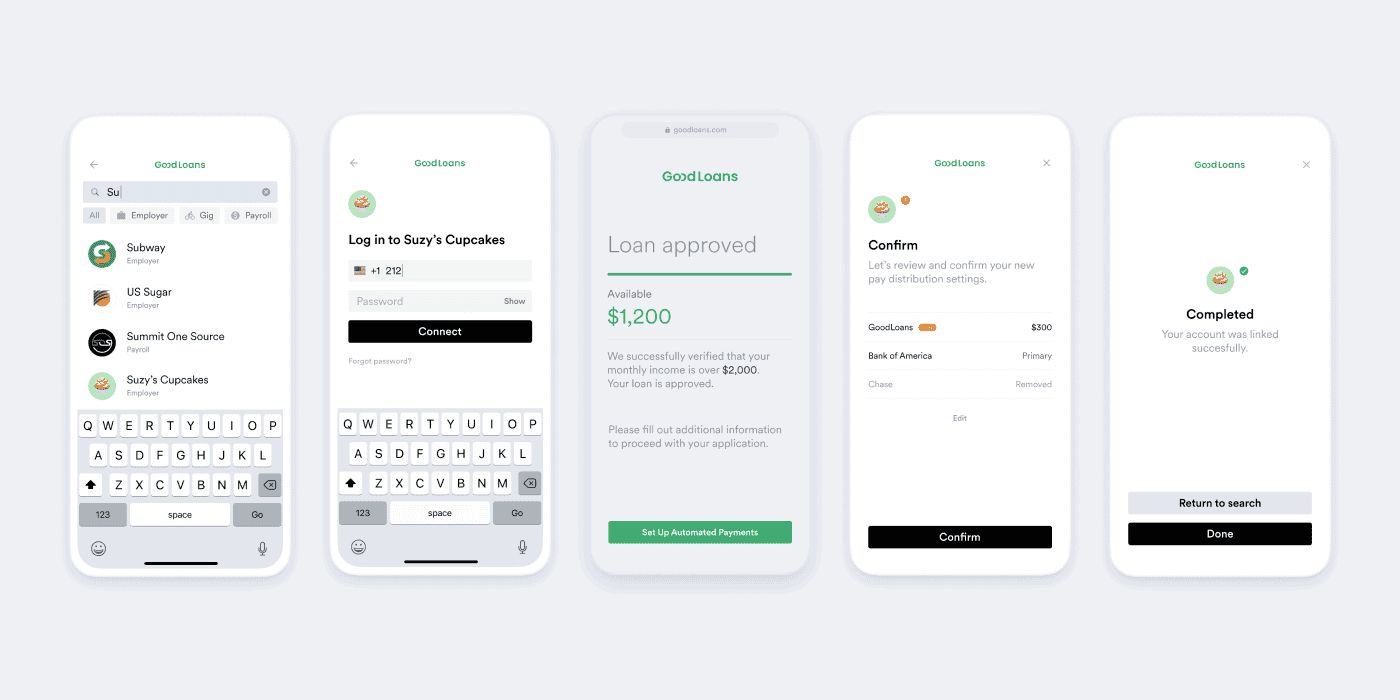

When implemented through a simple, automated solution like Argyle, paycheck-linked lending is a two-step process for end-users:

First, a borrower connects to their payroll provider using the same login credentials they use every day at work

A lender instantly checks eligibility for loans based on paychecks and cash flow with access to the rich data available from payroll systems

The borrower can automate repayments by authorizing distributions from their incoming paychecks each month

Handled by the right platform, the entire flow is quick and easy for everyone involved. API-based, embeddable products like Argyle’s integrate seamlessly with existing programs, so users can set up loan and repayment terms without ever leaving the lender’s app.

Get Started with Paycheck-Linked Lending for Free

Who it helps

For borrowers, paycheck-linked lending unlocks access to affordable small-dollar loans. These funds go toward everything from bridge funding for monthly bills to emergency expenses—like car breakdowns or unexpected medical bills. Paycheck-linked lending also lowers interest rates on larger debt consolidation loans or auto loans.

For lenders big and small, payroll distribution loan models mean more regular, reliable repayments and quicker, more confident lending decisions based on metrics that really matter instead of unreliable credit scores. Ultimately, it means lenders can serve and empower a wider swath of customers—without taking on additional risk.

How Argyle makes a difference

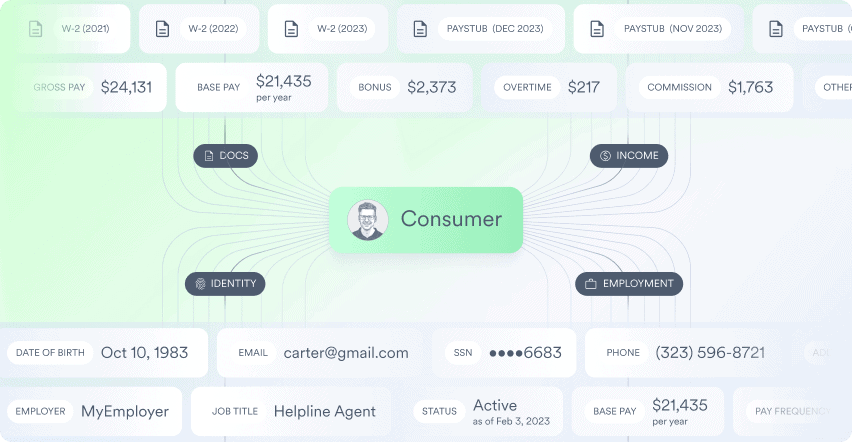

Argyle supports lenders and borrowers with real-time lending solutions that offer complete, user-permissioned access to users’ income and employment data and allows users to change the destination of their paychecks.

Argyle promises a number of immediate benefits, including:

Instant, automated onboarding: Users update their payroll system and automate repayments with a tap, avoiding the need for manual data entry, tedious ACH forms, and drawn-out, weeks-long approval processes

Continuous, transparent access: Lenders get ongoing visibility into borrowers’ income and employment data with their direct permission — including notifications whenever there’s a significant change

Comprehensive, standardized data sets: Argyle’s data package includes over 160 endpoints organized in an intuitive, accessible way, so customers can make more informed, confident lending decisions

Flexible, customizable integrations: Argyle’s solutions can be embedded directly into an app or linked through invitations sent to users via email or SMS — optimizing workflows and improving both the user experience and conversion

Building a paycheck-linked loan product is easier than ever with new partner, Highline

Highline was built to bridge the gaps between payroll and outstanding payments. With Argyle providing access to the paycheck, Highline manages the flow of funds to align with any existing product structure. Retrofitting a lending product for payroll payments can be like fitting a square peg into a round hole. Loans repaid from income are much lower risk, but the odd frequencies and limitations of direct deposits often create insurmountable challenges. With Highline, any lender or biller can receive payments from payroll without rearchitecting their products.

Highline’s platform addresses critical gaps for quick adoption, in addition to everything Argyle provides:

Lower technology investment: Get paid at any frequency, no FBO (“For benefit of,” a.k.a. custodial) accounts needed, no handling of excess payments, workflows for changes in income

Broader coverage: Get paid from the >20% of customers that can’t add a new direct deposit

Reduced regulatory risk: Accept payments from Reg B protected incomes, comply with state regulations on first payment grace period and frequencies

Want to learn more?

Read about how existing partner BMG Money uses Argyle’s paycheck-linked lending platform to streamline its underwriting tasks and automate repayments. Plus, visit the Argyle product page for a deeper look at how Argyle’s paycheck-linked lending solutions work across all kinds of lenders — and how they’re supported by Argyle’s automated Verification of Income and Employment and Direct Deposit Switching flows.

If you’re ready to reduce your default risk, sign up for a free corporate account, and give the sandbox a try.